The Task Force on Climate-related Financial Disclosures has been a game changer for corporations. The task force, created in 2015 at the behest of the G-20 countries, sets clear guidelines on climate risk disclosure for companies. It also helps to steer financial markets in pricing assets’ value and thus allocate capital accordingly.

The TCFD urges companies to use forward-looking scenario analysis as a tool in identifying climate-related risks. In introducing the final recommendations in 2017, the TCFD said it expected scenario analysis would be “a largely qualitative exercise,” but organizations with more experience in calculating climate risks were encouraged to conduct quantitative scenario analysis.

Quantitative scenario analysis uses analytical models to determine a wide range of climate-risk outcomes, while qualitative scenario analysis is based on descriptive narratives and is often the first step for organizations to explore potential future climate impacts.

The most recent TCFD report shows that companies remain hesitant about reporting quantitative data. From a sample of 25 companies reviewed in the TCFD’s 2021 status report, 20 disclosed financial risk “in a qualitative, directional, and aggregated” way, while quantitative disclosure was less common. “Discussion of physical impacts was typically in the form of qualitative descriptions rather than quantitative information,” the task force wrote.

The TCFD’s goal is to encourage companies to report on climate risk that is material to their business; otherwise, they are not giving a true picture of their financial accounts. TCFD supporters include investors with over $100 trillion in assets under management who need transparency from issuers about the financial risks they face from climate change. Accordingly, TCFD provides a framework for assessing and disclosing potential financial impacts from physical risks, which include increased flooding, more frequent hurricanes and wildfires, and transition risks, which refer to the business costs of market, policy, regulatory and technological changes.

However, quantifying climate risk is a very complex and specialized endeavor, requiring data, methodologies, and expertise beyond the core competencies of many corporations. For example, climate-related financial risk isn’t spread evenly like peanut butter. The risk is generally concentrated in certain types of assets, time periods and geographies. Companies within the same sector, with assets located in different locations, can have significantly different climate-related financial risks.

But companies need not be afraid of moving from a qualitative to a quantitative approach. In the five years since the TCFD published its recommendations, the data and methods that are used to model climate risk have dramatically matured.

The greatest advance in modeling physical climate risk has been in vulnerability models. These connect the degree of physical hazard (e.g., the severity of the flooding) to financial damage. Vulnerability models — sometimes called damage functions or impact functions — must be constructed for many different types of assets. For example, consider a severe region-wide drought. If an investor owns an office building and a vineyard right next to each other, experiencing the same severity of drought, the economic productivity of the office building might not be affected much at all, whereas the vineyard could be decimated.

Because different assets respond to the same hazard in different ways, and because the location of assets determines their exposure to hazards in the future, the asset-level data itself is key to the analysis. Then risks can be aggregated to the company and portfolio level, across multiple greenhouse gas emission scenarios and time horizons. High-quality asset data is the foundation for a bottom-up analysis.

Let’s look at another example – a bank.

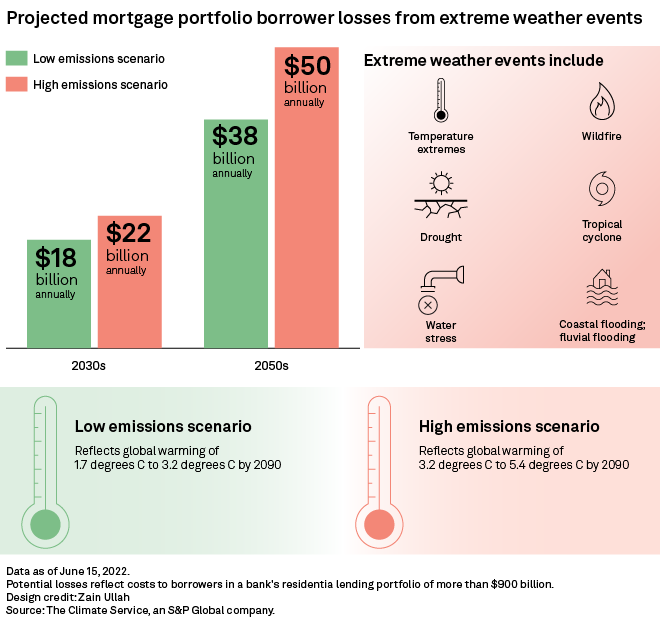

Consider the case of a multinational lender that wanted to model how climate change could affect its mortgage portfolio worth north of $900 billion. The lender was looking to model the potential future risks to both residential and commercial buildings associated with their mortgage loans. Gone are the days when these questions could be answered at the aggregate level, or with a simple map of higher temperatures. The bank wanted to know the specific financial impact of each type of physical climate hazard to each individual asset.

An analysis by The Climate Service, now a part of S&P Global, demonstrated that borrowers would face $22 billion in annual losses because of physical hazards in the 2030s under a high emissions scenario, which reflects 3.2 degrees C to 5.4 degrees C of warming by end of century. In the 2050s, these losses rise to $50 billion annually. Under a lower emissions scenario of between 1.7 degrees C and 3.2 degrees C by 2090, these annual losses remain substantial: $18 billion in the 2030s and $38 billion in the 2050s.

In the analysis, each asset is assessed against future material climate risks to calculate the average annual loss as well as the owner’s costs and loss of revenue as a percentage of the asset’s value. By quantifying future climate hazards, the bank used data-driven, science-based insights to help it manage climate-related financial risk.

By taking a quantitative approach to climate risks in financial reporting, companies can drill down into data on specific assets to discover where the climate hazards to their business models lie. It can protect them against future financial losses and help them avoid costly interruptions to their business and damage from extreme weather.

Five years on, TCFD has firmly established itself as a reporting framework. Many jurisdictions, including the U.K. and New Zealand, are making it mandatory for companies to report on climate risk, with many of them endorsing the TCFD. A strong signal for widespread compulsory TCFD disclosure came in June 2021, when the G7 group of countries said they supported the disclosure framework.

The rapidly evolving field of climate risk analytics is now giving corporations tools to model their climate-related financial risks in a quantitative — and therefore actionable — way. These tools can help companies begin making the switch from qualitative to quantitative assessments and disclosures, and to model, manage and monitor their climate-related financial risks.