The EU Taxonomy is an attempt to define what makes a “green” investment and is a cornerstone of the EU’s sustainable finance policy agenda. The Taxonomy can be thought of as a dictionary defining which economic activities can be considered environmentally sustainable.

The core question now facing companies, investors and financial institutions is how to identify Taxonomy-aligned activities and revenue. This blog describes the general approach the S&P Global EU Taxonomy Data Solution takes in assessing economic activities and revenue to determine their eligibility for the Taxonomy.

What are eligible activities, and how do they differ?

Taxonomy eligibility and Taxonomy alignment are not the same. Taxonomy eligibility is an assessment of whether an economic activity has a set of corresponding criteria in the Taxonomy to be assessed against — in other words, whether the activity is in scope of the Taxonomy to begin with. Taxonomy alignment is the positive assessment that an eligible activity meets the applicable Taxonomy requirements to substantially contribute to at least one of the Taxonomy’s six objectives; does no significant harm to any other objective; and meets the minimum safeguards.

The Taxonomy is not only used within its own regulatory framework for sustainable finance; it also serves as a reference for Sustainable Finance Disclosure Regulation (SFDR) product disclosures, for client sustainability preferences under the capital markets legal framework MiFID II and for some national regulations. For financial institutions, understanding which activities are eligible under the Taxonomy is the first step to assess the proportion of Taxonomy-aligned activities at an entity or product level, which in turn allows them to make regulatory disclosures.

The taxonomy defines sustainability at the individual economic activity level (e.g., cement manufacturing or hydrogen storage) rather than the company level. This means that companies themselves cannot be considered eligible, but some or all of their underlying activities may be.

For an activity to be considered eligible, it must be able to contribute to at least one of the Taxonomy’s six environmental objectives. The list of activities with the potential to contribute to two of the objectives — climate change mitigation and climate change adaptation — has been agreed; eligible activities related to the other four objectives will be finalized in the future.

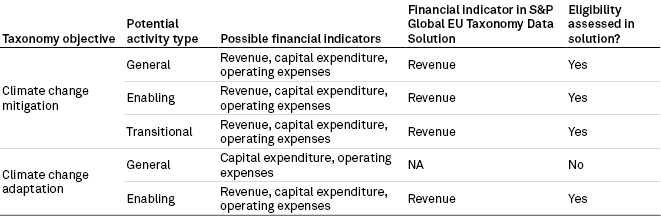

Beyond classifying eligible activities by their Taxonomy objective, activities can be further categorized by three types: whether they can contribute directly to a Taxonomy objective; only enable other activities that contribute directly; or are transitional, which can apply to some activities associated with the climate change mitigation objective that do not have a low-carbon alternative.

The first type includes activities that directly contribute to a Taxonomy objective. For instance, solar power generation may contribute directly to the climate change mitigation objective by providing zero-emissions electricity and helping mitigate the rise of greenhouse gas levels in the atmosphere. In the S&P Global EU Taxonomy Data Solution, these are called “general” activities.

The second type of activities includes those that have the potential to enable other activities to contribute directly to one of the objectives. Manufacturing solar panels, for example, may enable solar power generation to contribute to climate change mitigation, but the manufacturing process itself does not directly contribute.

The third type of activity to consider is a transitional activity under the climate change mitigation objective. These are activities that aren’t typically considered “green” or “sustainable,” but that have no technologically or economically feasible low-carbon alternatives. If the activity has best-in-sector greenhouse gas emissions and does not hamper the development or deployment of low-carbon alternatives, the Taxonomy views it as having the potential to make a substantial contribution to climate change mitigation and reaching the Paris Agreement goal of limiting global warming to 2 degrees C above preindustrial levels and ideally to no more than 1.5 degrees C. Activities such as the manufacture of cement may fall under this potential activity type.

Activities must also meet a set of technical screening criteria before they can be considered enabling or transitional. These activities should be referred to as “eligible-to-be-enabling” or “eligible-to-be-transitional” until they have been shown to meet the criteria, the European Commission has said.

The S&P Global Sustainable1 approach to assessing eligibility

A company often engages in multiple economic activities, and they all need to be assessed individually for eligibility. The Trucost Sector Revenue dataset separates each company’s total revenues into their individual economic activities and associated revenues using company-reported information.

This dataset covers more than 20,000 companies, accounting for 99% of global market capitalization, and uses the Trucost Sector Activities Classifications to divide the entire economy into 464 business activities. Of these, 176 were mapped to NACE[1]-based eligible activities as defined by the EU Taxonomy. We also include the climate objective to which the activity contributes and the potential activity type it could be assigned if technical screening criteria is met.

Revenue is the metric used to assess activity types for the mitigation and adaptation objectives, with one exception: general adaptation activities. Directly contributing to climate change adaptation often reflects a company’s spending on projects that reduce climate change physical risk, rather than generating revenue. As a result, general adaptation is currently best measured by capital expenditure rather than revenue.

However, because there is limited capital expenditure disclosure at the activity level, the S&P Global EU Taxonomy Data Solution does not assess the general adaptation activity type. An adaptation enabling activity, on the other hand, is often a result of a business activity that generates revenue — for example, providing consultancy services to another company that allows it to adapt its business to prepare for physical climate risk. That means it can be assessed using revenue as the eligibility metric.

Taxonomy objectives and activity types

Data as of Sept. 14, 2022.

NA = not applicable

Source: S&P Global Sustainable1.

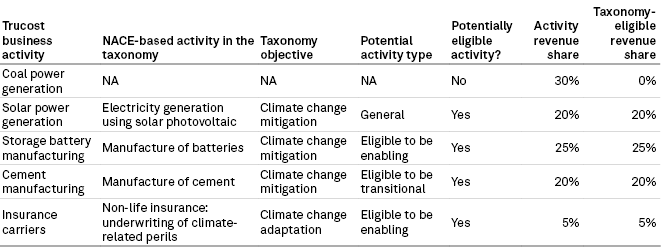

Once a company’s economic activities have been individually assessed for eligibility, they must be re-aggregated at the company level. We use the activity-level revenue data from our dataset to calculate the company-level eligible revenue share. For example, for this hypothetical company with very different business activities, a total of 70% of its revenue is Taxonomy-eligible across two objectives.

Assessing Company A’s Taxonomy-eligible revenue

Data as of Sept. 14, 2022.

NA = not applicable; NACE = Statistical Classification of Economic Activities in the European Community

Source: S&P Global Sustainable1.

This company-level data can be further aggregated at the portfolio or index level based on climate objective and potentially eligible transitional or enabling activity type.

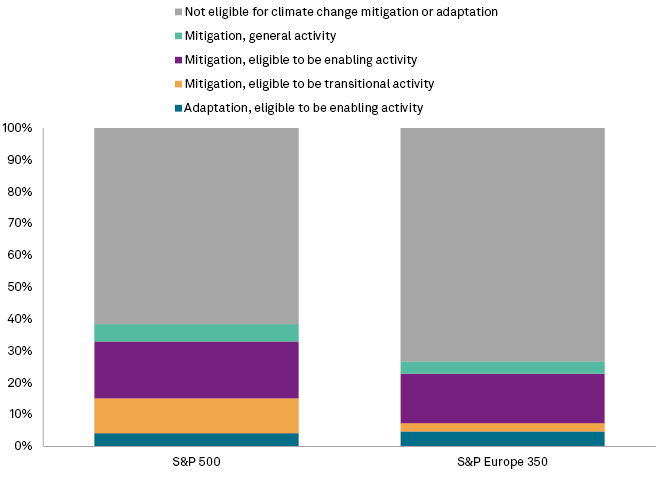

Breakdown of Taxonomy-eligible revenue share in S&P 500 and S&P EUROPE 350 by climate objective and potential activity type

Index data as of July 26, 2022.

Trucost Sector Revenue and Trucost Sector Activities Classifications reflect full-year 2020, the latest available data.

Source: S&P Global Sustainable1.

Is it always better to have more eligible revenues?

While it is tempting to assume that having a higher percentage of eligible revenues within a portfolio makes it “greener” or more “sustainable,” this is not necessarily the case.

Many of the sectors prioritized for inclusion under the climate change mitigation objective are high-emissions sectors that have a significant need for decarbonization under the currently agreed Paris Agreement climate targets. The sectors selected as eligible in the EU Taxonomy accounted for a minimum of 93.5% of the EU’s NACE-based Scope 1 emissions in 2018, according to the EU. Within these sectors, policymakers chose activities with a wide range of emissions levels, from very high emitters with the potential for large emissions reduction to activities with low emissions to begin with.

Focusing on revenue eligibility is only the first step to assessing actual alignment with the Taxonomy. To contribute to one of the Taxonomy’s objectives, an economic activity must also meet requirements for substantial contribution, doing no significant harm to other objectives and complying with minimum social safeguards. Examining these three requirements — the next steps in determining Taxonomy alignment — will be the focus of future parts of this blog series.

[1] NACE, or Nomenclature statistique des Activités économiques, is the statistical classification of economic activities in the EU.