Regulation is shaping the sustainability agenda and changing the way companies do business in different jurisdictions, but keeping pace with constant regulatory updates has become a mammoth task for businesses and investors. In this recurring series, S&P Global Sustainable1 presents key environmental, social and governance regulatory developments and disclosure standards from around the world.

In this month's update, we look at proposals for sustainability disclosures from three Chinese stock exchanges, the EU’s recommendations for cutting greenhouse gas (GHG) emissions and Singapore’s adoption of disclosures aligned with the International Sustainability Standards Board (ISSB).

Europe

European Commission recommends cutting emissions 90% by 2040

The European Commission on Feb. 6 recommended setting a new target to reduce net GHG emissions 90% by 2040 relative to 1990 levels as part of the EU's broader goal of achieving net-zero by 2050. Meeting the 2040 target would require hitting the EU's existing goal to cut emissions by at least 55% by 2030, the Commission wrote, adding that setting a target for 2040 "will send important signals on how to invest and plan effectively for the longer term, minimizing the risks of stranded assets." The 2040 proposal includes a "greater focus on a just transition that leaves no one behind" and includes a strategic dialogue with industry and the agricultural sector. A legislative proposal is expected to be presented by the new Commission following European elections in June 2024. The commission also released a related industrial carbon management plan to help achieve the new target through the use of carbon capture and investments in technologies that remove carbon from the atmosphere.

EU lawmakers strike deal on Net-Zero Industry Act

The European Parliament and the Council of the EU on Feb. 6 provisionally agreed on the European Commission’s plan to boost the manufacturing of clean technologies within the EU and reduce the bloc’s dependence on imports. The Net-Zero Industry Act (NZIA) envisages 40% of EU demand for net-zero technologies, such as wind turbines and solar panels, being met by local manufacturing by 2030. To increase the competitiveness of EU products, the NZIA "requires public authorities to consider sustainability and resilience criteria" for some procurement processes, the Commission said. That could include social responsibility, cybersecurity or timeliness in delivery. These criteria will apply to at least 30% of the volume of renewables auctioned yearly. The act aims to reduce administrative and permitting requirements, including via Net-Zero Acceleration Valleys, where member states can create industrial clusters with streamlined processes. The plan also supports the development of carbon capture and storage activities in the EU, funded by contributions from oil and gas producers on a pro-rata basis related to fossil fuel production. The Commission said its objective was to reach 50 million metric tons of capacity injected in geological storage sites annually by 2030.

EU reaches provisional agreement on regulation of ESG rating providers

The European Parliament and the Council of the EU, composed of government ministers of the 27 EU member states, reached a provisional agreement on Feb. 5 over the regulation of ESG rating providers. Under the provisional agreement, EU-based ESG rating providers would need to receive an authorization from the European Securities and Markets Authority (ESMA). ESMA would supervise ESG rating providers, and providers would need to comply with requirements related to transparency in the ratings’ methodology, the Council said. ESG rating providers not based in the EU but seeking to operate in the EU would need an EU-authorized ESG rating provider to endorse their ESG ratings, the council said. The provisional agreement about the regulation is still subject to approval by the Council and Parliament. It would apply 18 months after it enters into force.

EU lawmakers reach agreement on delaying sector-specific sustainability reporting standards

The European Parliament and the Council of the EU on Feb. 7 reached a provisional agreement on postponing the adoption of the European Sustainability Reporting Standards (ESRS) for specific sectors and non-EU countries by two years to June 30, 2026. The council said the decision would allow companies to focus on the implementation of the first set of ESRS, adopted by the European Commission on July 31, 2023. Those standards cover a range of topics including climate change, biodiversity and human rights. The council also said the agreement would allow more time to develop sector-specific sustainability standards as well as standards for third-country companies that have annual revenues of €150 million in the EU and at least one subsidiary or branch in the EU. The agreement also encourages the commission to publish the eight sector-specific reporting standards as soon as they are ready before the new deadline on June 30, 2026. The ESRS apply to companies that are subject to the EU's Corporate Sustainability Reporting Directive (CSRD).

EU legislators agree on carbon removals certification framework

The European Parliament and the Council of the EU on Feb. 20 reached a provisional political agreement on establishing an EU-level certification framework for carbon removals. The regulation differentiates among several carbon removal activities, including permanent carbon removal, or storing carbon for several centuries; temporary carbon storage in long-lasting products such as wood-based construction for at least 35 years; temporary carbon storage from carbon farming such as restoring forests and soil, wetland management or seagrass meadows; and emission reductions from soil management. The proposed framework can be used to certify removals that employ any of these approaches, the EU said, and certification will depend on four aspects of a removal project: quantification, additionality, long-term storage and sustainability. The European Commission will develop tailored certification methodologies for different types of carbon removal. It will also establish an electronic EU-wide registry four years after the entry into force of the regulation, the Council said.

ASIA-PACIFIC

Chinese stock exchanges propose sustainability reporting guidelines for listed companies

Shanghai Stock Exchange (SSE), Shenzhen Stock Exchange (SZSE), and the Beijing Stock Exchange (BSE) proposed on Feb. 8 sustainability reporting guidelines for listed companies to help standardize and improve the quality of sustainability-related disclosures by listed companies. The SZSE said companies listed on the blue-chip Shenzhen 100 Index and the tech-focused ChiNext Index would be subject to mandatory disclosure while other listed companies will be encouraged to report voluntarily. The SSE said companies listed on the blue-chip SSE 180 Index and SSE Science and Technology Innovation Board 50 Index would be required to report. The disclosure requirements include key themes such as governance, strategy, impact and risk and opportunity management. Companies would be required to report on carbon emissions, pollutants, ecosystem and biodiversity, circular economy utilization, rural revitalization and supply chain security governance, the exchanges said. Companies listed on the BSE would disclose on a voluntary basis.

China announces plan to expand carbon market

China’s Ministry of Ecology and Environment announced plans on Feb. 27, 2024, to expand its carbon market to a total of eight major carbon-emitting industries from one. The ministry plans to add seven industries, including steel, building materials and nonferrous metals, to the market, which is currently open to only the power generation sector. The eight industries would account for 75% of the country’s emissions, the ministry said. It also said it had completed drafts on how to incorporate the additional seven industries, including how to allocate carbon emission allowances and compile reports on carbon accounting verification.

Malaysia’s sustainability reporting body holds consultation on ISSB adoption

Malaysia’s Advisory Committee on Sustainability Reporting launched a consultation on Feb. 15, 2024, on proposals for adopting the first two sustainability disclosure standards issued by the International Sustainability Standards Board (ISSB) in June 2023. Malaysia plans to adopt the standards as of 2025 from 2025-2026 for main market-listed companies, and from 2027-2028 for companies listed on Malaysia's ACE high-growth market and non-listed large companies with annual revenues of 2 billion ringett or more. Main market-listed issuers would be required to disclosure under the ISSB’s IFRS S2 Climate-related Disclosures for the 2025 financial year, with relief on some disclosures. For example, they would have the option not to disclose the impacts of climate-related risks and opportunities on the company’s strategy and decision-making. They would also be exempt from reporting on Scope 3 greenhouse gas emissions, which are the indirect emissions that occur up and down a company's value chain. Main market-listed companies would be subject to the ISSB’s IFRS S1 General Requirements for Disclosure of Sustainability-related Financial Information for financial year 2026, with reliefs. The ISSB decided in April 2023 that companies can take a phased-in approach to reporting under its standards, allowing them to focus only on climate-specific information the first year of reporting. Main market-listed companies would be required to adopt both standards fully from financial year 2027. The consultation ended on March 29, 2024.

Singapore adopts climate-related reporting disclosures based on ISSB standards

Singapore's Accounting and Corporate Regulatory Authority and Singapore Exchange Regulation announced on Feb. 28, 2024, plans to phase in mandatory climate reporting for listed issuers and large non-listed companies. All listed issuers will be required to report and file annual climate-related disclosures from 2025, including Scope 1 emissions, which come from direct operations, and Scope 2 emissions, which are indirect emissions primarily derived from purchased energy. Issuers will apply disclosure requirements aligned with the ISSB standards, the authorities said. They will be required to report on Scope 3 emissions from 2026 and provide limited external assurance on their Scope 1 and Scope 2 emissions from 2027. Large non-listed companies with annual revenue of at least S$1 billion and total assets of at least S$500 million will start mandatory climate reporting, including Scope 1 and Scope 2 emissions from 2027. They will report on Scope 3 emissions no earlier than 2029 and provide limited external assurance on their Scope 1 and Scope 2 emissions from 2029.

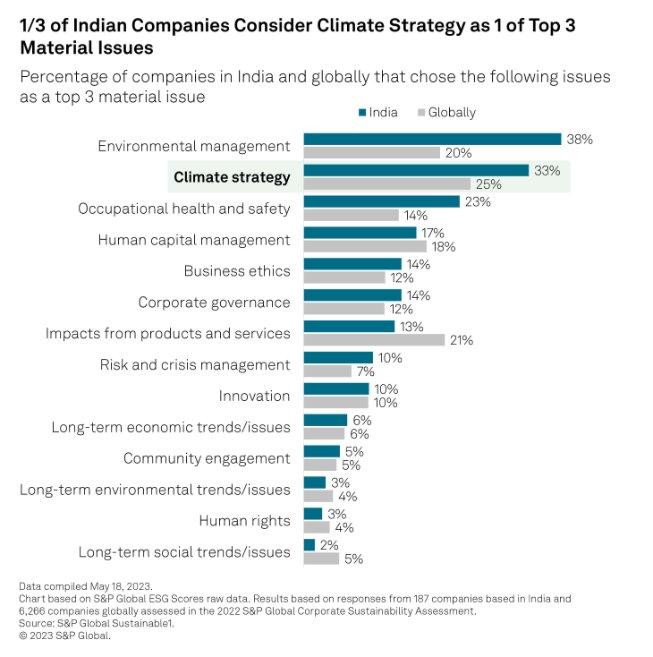

Reserve Bank of India proposes climate-related disclosure framework for financial institutions

India's central bank, the Reserve Bank of India, published on Feb. 28, 2024, a draft framework for banks and financial institutions to disclose climate-related risks. The disclosure framework is based on the ISSB’s standards. Banks and financial institutions would be required to disclose their climate risks related to governance, strategy and risk management from fiscal year 2025–2026 and for metrics and targets from fiscal year 2026-2027, in accordance with the ISSB’s IFRS S1 General Requirements for Disclosure of Sustainability-related Financial Information. They would have to report on the governance processes, controls and procedures used to identify, assess, manage, mitigate, monitor and oversee climate-related financial risks. They would also be required to outline their strategy for managing these financial risks and any targets they are required to meet by statute or regulation, the central bank said. The RBI is holding a consultation on the draft disclosure framework until April 30.

AFRICA

Nigeria publishes draft roadmap for adoption of ISSB standards

The Financial Reporting Council of Nigeria, a government agency that oversees financial reporting standards, announced on Feb. 3, 2024, a consultation on its draft roadmap for adoption of ISSB sustainability-related disclosure standards. Nigeria adopted standards as of Jan. 1, 2024, to be voluntary until 2026. Mandatory reporting would be phased in from 2027. Significant public interest entities, which include listed and non-listed regulated companies, would report from 2027, public interest entities from 2028 and small-and-medium-sized entities from 2030. The council plans to conduct a readiness test to ascertain companies’ preparedness for adoption of the standards, and companies would be required to submit information on their implementation plans, their IFRS S1 and S2 accounting policies and identification of sustainability and climate-related risks and opportunities, among other things. Companies would have to consider sustainability-related material risks, governance, strategy, risk management, metrics such as Scope 1, Scope 2 and Scope 3 emissions, as well as climate-related transition and physical risks and quantitative and qualitative climate-related targets in their adoption of the standards. Transition periods would align with ISSB guidelines, such as providing a one-year exemption for Scope 3 reporting. The consultation closed on March 14, 2024.

This piece was published by S&P Global Sustainable1 and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Navigate the regulatory landscape with essential intelligence |

This list is not exhaustive, and information is current as of the publication date. If there are additional significant regulatory developments we should cover going forward, please reach out to Jennifer Laidlaw at jennifer.laidlaw@spglobal.com. We welcome feedback.