Regulation is shaping the sustainability agenda and changing the way companies do business in different jurisdictions, but keeping pace with constant regulatory updates has become a mammoth task for businesses and investors. In this recurring series, S&P Global Sustainable1 presents key developments on regulations and potential disclosure standards from around the world.

In this month’s update, we look at the U.S. Securities and Exchange Commission’s sweeping climate disclosure proposal, how corporate sustainability reporting rules and a carbon border levy are making their way through the EU legislative process and New Zealand’s efforts on developing its own climate disclosure standards by the end of 2022.

International United States and Canada Europe Asia-Pacific

International

ISSB releases proposals for climate disclosures

The newly formed International Sustainability Standards Board, or ISSB, published exposure drafts of its first two proposed standards on March 31. The move is an early step in creating uniform global ESG standards and could simplify disclosure for investors and corporates amid the proliferation of different sustainability reporting frameworks. Once finalized, the ISSB’s standards could be adopted by regulators as they build out disclosure regimes. The ISSB’s proposed climate standard would require companies to disclose information on their climate-related exposure and their strategy for addressing climate risks. Under the board’s general requirement disclosure proposal, companies would have to provide information on sustainability-related risks to investors, lenders and other creditors to help them assess a company’s total value. The proposals build on the work of the Task Force on Climate-related Financial Disclosures and the Sustainability Accounting Standards Board. Several countries have passed legislation to make TCFD disclosures mandatory. The ISSB is seeking comment before July 29 and will aim to publish the standards by the end of 2022.

Biodiversity taskforce releases draft framework

The Taskforce on Nature-related Financial Disclosures released a draft version of its reporting guidelines designed to help corporations, investors and lenders account for nature-related risks. It said more than half of the world’s economic output, or $44 trillion, depends on nature. Companies are failing to consider how their business impacts nature, while lenders and investors are not assessing nature-related risks in their lending and investment portfolios, the TNFD said. The framework sets out definitions of natural capital, proposed disclosure recommendations and a process for assessing nature risk. The TNFD’s goal is to finalize the framework by the end of 2023 after gathering feedback. The Taskforce is not a regulatory body, but its recommendations could be adopted by regulators as they expand climate-related disclosures in their jurisdictions.

United States and Canada

U.S. SEC proposes sweeping climate disclosure standards

The U.S. Securities and Exchange Commission, which oversees the world’s largest financial market, proposed on March 21 sweeping new climate disclosure standards. Under the proposal, SEC-registered public companies would have to annually report the greenhouse gas emissions created directly by their business activities and indirectly by their purchased energy — known as Scope 1 and Scope 2 emissions. They would also be required to report Scope 3 emissions up and down their value chains if they deem Scope 3 to be material. The proposal, which includes several other major disclosures, is currently open for comment. The SEC also described a potential phase-in timeline over several years for different aspects of the proposal.

Read more about the SEC’s proposal here.

Europe

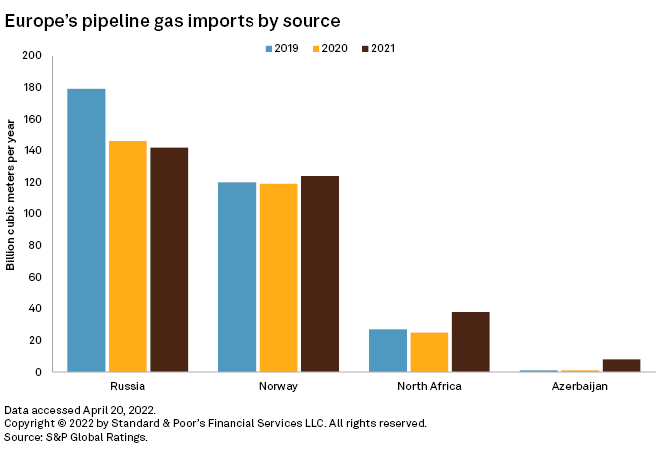

European Commission looks to speed up renewables transition to cut reliance on Russian gas

The European Commission, the EU’s executive arm, on March 8 proposed an outline of a plan to speed up the bloc’s clean energy transition and reduce its dependence on Russian gas. Under the proposal, member states would diversify gas supplies, increase biomethane and renewable hydrogen production and imports as well as replace gas in heating and power generation. The proposal aims to cut demand for Russian gas by two-thirds by the end of 2022 and phase out dependence on Russian fossil fuels. The EU imports 90% of its gas needs, with almost half of that coming from Russia. European Commission President Ursula Von der Leyen said on March 11 the Commission would publish in mid-May a proposal to phase out Russian oil, gas and coal by 2027.

EU Council adopts corporate sustainability reporting regulation proposals

The Council of the European Union, made up of government ministers from the 27 EU member states, formally adopted its position on the European Commission’s proposals for the reform of its corporate sustainability reporting rules. The move means discussions will start on the proposal in the European Parliament in spring 2022. The European Parliament announced on March 15 that its legal affairs committee had adopted its position on the reform, which aims to transform the current Non-Financial Reporting Directive into the Corporate Sustainability Reporting Directive, or CSRD. The CSRD would expand the reporting requirements and increase the number of companies disclosing on environmental and social issues. It also anchors the idea of “double materiality,” in which firms need to think of reporting not just in financial terms but also in terms of how their business affects the environment, its workers and its end-customers. The Commission could adopt the general standards by Oct. 31, 2022 and sector-specific standards by Oct. 31, 2023. The Council suggested pushing back the implementation of the reform by corporations for a year, meaning companies already subject to the NFRD would report for the first time in 2025 based on 2024 data.

EU Council agrees to move forward on carbon border levy

The European Council agreed on March 15 to the European Commission’s proposed carbon border adjustment mechanism, or CBAM. The mechanism would place a levy on imports from countries where carbon prices are lower than those in the EU or nonexistent — in other words, where goods can be produced without accounting for the hidden costs of contributing to greenhouse gas emissions. The European Commission presented the mechanism in July 2021 as part of a broad climate package named Fit for 55 designed to reduce carbon emissions by 55% compared with 1990 levels by 2030. The Council largely agreed with the Commission proposal, but opted for more centralized CBAM oversight, with a new registry of CBAM importers to be housed at the EU level, instead of by individual EU member states. It also said further work was necessary on how to phase out free allowances allocated under the EU’s Emissions Trading Scheme, among other issues. The Council will start negotiations with the European Parliament once the parliament has decided on its own position.

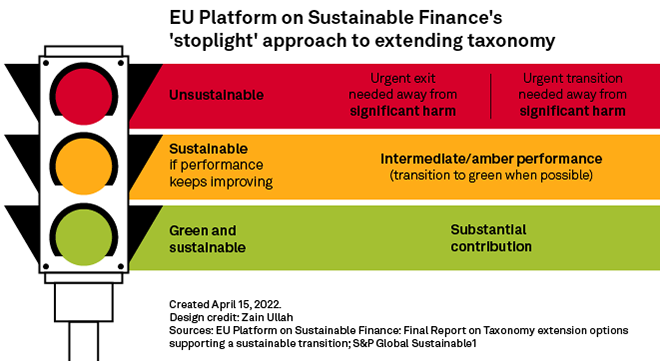

European Commission advisory group proposes ‘traffic light’ system to extend taxonomy

The EU Platform on Sustainable Finance, which advises the European Commission on sustainable finance regulations, on March 29 proposed extending the EU taxonomy to include a wider range of economic activities that may not be able to reach the green performance level defined by the taxonomy but still need to transition to more sustainable models. Under the proposal, some hard-to-abate sectors could benefit from taxonomy-recognized investment to help them become greener. Using what the proposal described as a “traffic light” approach, economic activities classed as green would make a substantial contribution to the EU’s environmental goals “Red” activities would do significant harm, while “amber” ones would be sustainable if they kept improving their environmental performance. The recommendation also includes a “low environmental impact” classification to include activities that do not harm the environment, but cannot be classed as green, amber or red. In related news, the platform released another report on March 30 defining criteria for the taxonomy’s four remaining environmental objectives: water and marine protection; circular economy; pollution prevention; and biodiversity. Reporting revenue aligned with these four objectives will apply from Jan. 1, 2023.

European Commission takes on fast fashion as part of its circular economy plan

The European Commission on March 30 announced a package of proposals aimed at making consumer goods such as clothes and smartphones more durable, more recyclable and more energy efficient, as part of its circular economy plan. Textile products sold in the EU by 2030 would have to be made “as much as possible” from recycled fibers and manufactured in respect of the environment and workers’ social rights. The Commission also set out plans for making the construction sector more sustainable, noting that buildings account for 40% of EU's energy consumption and 36% of energy-related greenhouse gas emissions.

EU supervisory bodies ask market participants to quantify taxonomy alignment of investments

The three European Union supervisory authorities – the European Banking Authority, the European Securities and Markets Authority and the European Insurance and Occupational Pensions Authority – are asking financial market participants to quantify what percentage of their investments underlying a financial product are taxonomy aligned, according to updated guidance on taxonomy disclosures and the Sustainable Finance Disclosure Regulation published on March 25.

Asia-Pacific

New Zealand reporting body expects to issue climate standards by December 2022

New Zealand’s External Reporting Board, or XRB, which establishes financial reporting standards, plans to publish a draft of new climate-related disclosure standards in July 2022 following a consultation on the document which closes on April 13, 2022. The move comes after New Zealand in 2021 became the first country to introduce mandatory "comply or explain" disclosures based on the voluntary Task Force on Climate-Related Financial Disclosures from 2023 for large financial institutions. The ongoing consultation focuses on climate strategy, metrics and targets, while a previous consultation in October 2021 covered governance and risk management. According to the board’s proposals, listed companies with a market capitalization of more than NZ$60 billion and financial institutions with assets of more than NZ$1 billion would have to report on their climate-related risks over the short, medium and long term as well as disclose the metrics they use to measure climate exposure. Corporations would also need to report on Scope 3 emissions, which include emissions from suppliers. The body said it expects to issue a standard by December 2022.

Australian finance group developing sustainable finance taxonomy

The Australian Sustainable Finance Initiative is seeking to build out an advisory group to help develop a sustainable finance taxonomy in 2022. The taxonomy will seek to set common definitions for sustainable economic activities and will be used to define sustainable investments. The taxonomy will build on taxonomies in the EU, Japan and Singapore, and on a common ground taxonomy created by the International Platform on Sustainable Finance, an international body seeking to scale up capital toward sustainable investments. The initiative is an industry group, but its work on a taxonomy has the support of Australia’s Council of Financial Regulators.

Taiwan’s financial market regulator sets out ESG strategy for securities market

Taiwan’s financial regulator, the Financial Supervisory Commission, on March 8 set out plans to make Taiwanese companies, investment firms and the securities market more sustainable as the country seeks to become carbon neutral by 2050. According to the commission’s strategy, companies would embed environmental, social and governance issues within their strategy and ensure the accountability of their boards of directors and management. Underwriters and consultants would assist listed companies in becoming more ESG-focused. The regulator will also set out frameworks for climate and sustainability disclosure. It said it plans to have the strategy in place in three years, working in conjunction with the Taiwan Stock Exchange, Taipei Exchange, Taiwan Futures Exchange, and Taiwan Depository & Cleaning Corporation.

This piece was published by S&P Global Sustainable1 and not by S&P Global Ratings, which is a separately managed division of S&P Global.

This list is not exhaustive, and information is current as of the publication date. If there are more significant regulatory developments we should cover going forward, please reach out to Jennifer Laidlaw at jennifer.laidlaw@spglobal.com. We welcome feedback.