Authors: Matt MacFarland | Marco Galbiati Stella | Esther Whieldon

Contributors: Seth Morrison, Drew Fryer, Jessica Taylor, Greg Wallace

Published: June 7, 2022

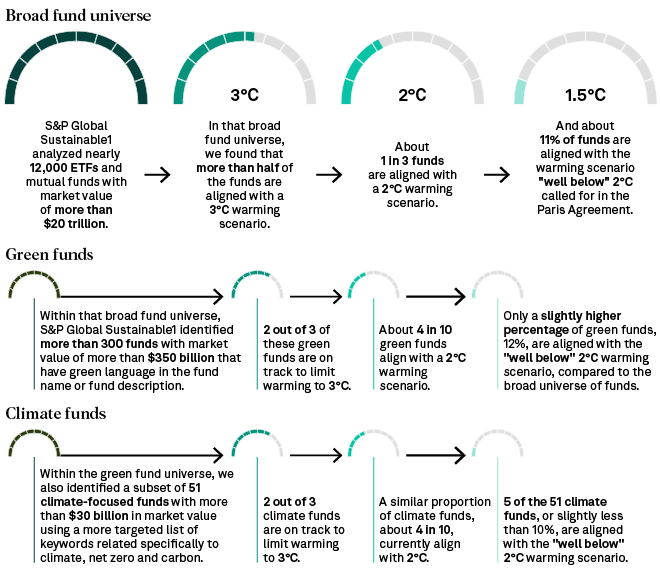

From a universe of nearly 12,000 equity mutual funds and exchange-traded funds representing more than $20 trillion in market value, S&P Global Sustainable1 found that about 11% are currently aligned with the Paris Agreement goal of limiting global warming to “well below” 2°C.

The analysis also identified more than 300 funds that use green or environmental language in their names or to describe their approach, as well as a subset of 51 climate-focused funds. Only about 12% of green funds are on budget to meet the goal of the Paris Agreement — nearly the same proportion as the broader universe of funds. An even smaller proportion of climate-focused funds are aligned.

While many green and climate funds are over budget on emissions, green funds as a group are slightly closer to Paris alignment than the broad fund universe, and by a statistically significant amount.

One in three green funds and climate funds are on a trajectory to overshoot even a less ambitious 3°C warming scenario, in which flooding, drought and sea level rise would pose severe risks to human life and society.

The findings provide a snapshot of the current state of equity investing — showing there is a long way to go toward aligning investor capital with the pathway that averts the worst consequences of climate change.

Equity mutual funds and exchange-traded funds around the world use green language to signal that their portfolios support the energy transition, address environmental concerns or combat climate change. But wide misalignment with the Paris Agreement goal of limiting global warming is the current reality for most of these funds, according to a new analysis by S&P Global Sustainable1 — and this could undermine the eco-friendly or climate-conscious signals they send to investors.

Under the Paris Agreement, more than 190 parties committed to limiting the global rise in greenhouse gas emissions to “well below” 2°C, and preferably 1.5°C, relative to preindustrial levels. The agreement brings together nations from around the world to work toward a common climate goal. Limiting warming to this target means reaching net zero emissions by midcentury.

Our analysis shows that based on current trajectories, equity funds across the board have a long way to go to meet the goal of the Paris Agreement. We started with a global universe of nearly 12,000 equity mutual funds and exchange-traded funds representing more than $20 trillion in market value. We then overlaid S&P Global Trucost Paris Alignment data covering more than 17,000 companies on the fund holdings to assess the funds’ warming trajectory. This data sums actual Scope 1 and Scope 2 emissions from 2012 to the most recent available historical data, and then forecasts emissions through 2025, comparing trends in those emissions with the rates of decarbonization that would enable achievement of different temperature scenarios.

The analysis then takes an additional step of calculating the budget alignment per $1 million invested, which puts the budget in perspective relative to the size of the portfolio's total market value as a measure of the investor's responsibility. The analysis does not name specific funds as the findings point to misalignment across the green fund cohort and across the broader universe.

Within that broad fund universe, we identified more than 300 funds representing more than $350 billion in market value that use green or environmental language in their fund names or to describe their investment objectives. Within that green fund universe, we also identified a subset of 51 climate-focused funds using a more targeted list of keywords related specifically to climate, net zero and carbon. Many funds rely on sustainability language to attract environmentally conscious, climate-conscious or global warming-conscious investors. As climate change increases in urgency, understanding decarbonization pathways becomes increasingly important — even for funds that don't explicitly state Paris alignment as a goal.

Data as of April 19, 2022.

Analysis uses S&P Trucost Paris Alignment data to assess the difference between a company's projected pathway for Scope 1 and Scope 2 greenhouse gas emissions and the required pathway to reach alignment with three different goals from 2012 to 2025. The most ambitious is a goal of limiting warming to "well below" 2°C, or 1.5°C. The second is a goal of limiting warming to 2°C. the third and least ambitious is a goal of limiting to 3°C.

Sources: S&P Global Trucost; S&P Global Sustainable1

We found that approximately 11% of the broad fund universe is on track to limit global warming to “well below” 2° above preindustrial levels by the year 2100. The data for our analysis treats the term "well below 2°" as equivalent to 1.5°, which is the target scientists say the world must hit to avoid the worst impacts of climate change.

For the green fund universe, results were only slightly better. Approximately 12% of green funds representing about $31 billion in market value were under their carbon budgets in a scenario of limiting global warming to “well below” 2°. In the smaller climate fund group, only one in 10 were aligned with 1.5° based on their current holdings.

The data suggests that the fund holdings are struggling to keep their emissions in check. This analysis does not purport to measure whether funds are mislabeled, are seeking to mislead investors or are engaging in greenwashing. Indeed, many of the over-budget green funds analyzed exclude fossil fuels, have a focus on renewables, or invest in companies driving the energy transition forward, such as electric vehicle manufacturers or climate technology solutions.1 Few funds state Paris alignment as a goal, and funds may have a wide array of other green objectives that benefit the environment or help address climate change. Some funds also seek to invest in and engage with emissions-heavy companies, using their clout as shareholders to direct companies toward decarbonization. Carbon transition indices may also include heavy emitters but be designed to rebalance in favor of constituents that make progress on decarbonization over time.

Even so, green funds as currently constructed are widely over budget according to the Trucost data forecasts through 2025, suggesting that many of their holdings are behind schedule in controlling their emissions and sourcing greener energy. A company or fund could satisfy its own definition of climate-conscious or green without being Paris aligned. But a fund that presents itself as climate-friendly because of fossil fuel exclusion or a focus on renewable energy but does not measure alignment with the 1.5° or 2° pathway (and could be misaligned even against a less ambitious 3°C warming scenario) is arguably missing the forest for the trees.

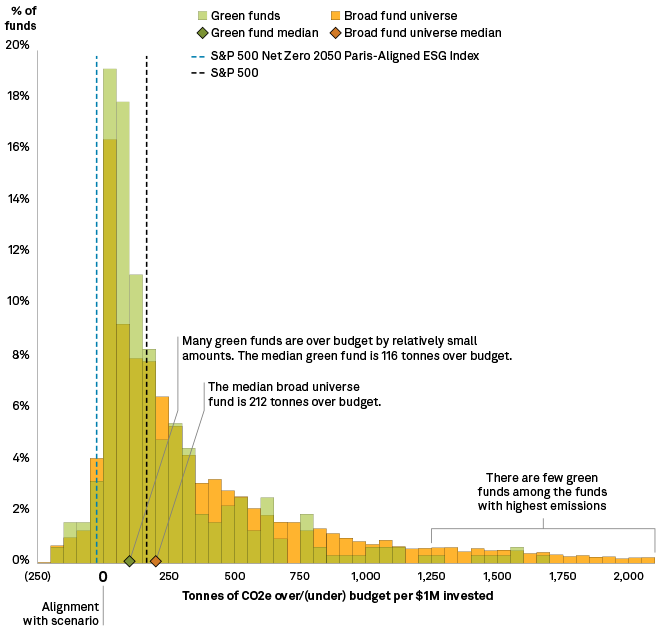

Toggle among the warming scenarios and fund comparisons to see the change in the number of funds that are over or under their emissions budgets, then hover over the bars for more detail.

Data as of April 19, 2022.

Analysis uses S&P Global Trucost Paris Alignment data to assess the difference between a company's projected pathway for Scope 1 and Scope 2 greenhouse gas emissions, and the required pathway to reach alignment with three different goals from 2012 to 2025. The most ambitious is a goal of limiting warming to "well below" 2°C, or 1.5°C. The second is a goal of limiting warming to 2°C. The third and least ambitious is a goal of limiting warming to 3°C.

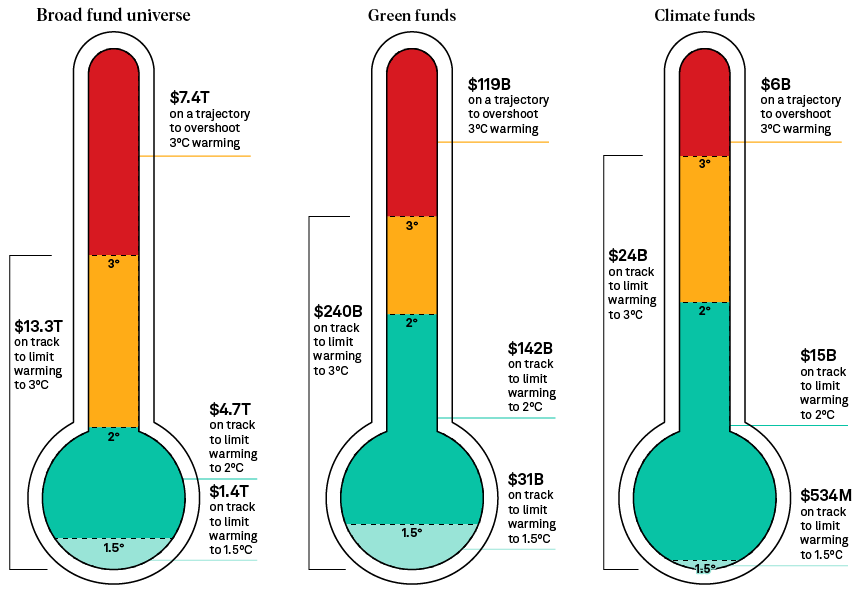

The broad fund universe represents 11,780 equity funds. The subset of green funds represents 334 funds. The climate funds subset of green funds represents 51 funds. Outliers were excluded to improve visibility of the distribution.

Sources: S&P Global Trucost, S&P Global Sustainable1

This issue is front and center as the trend of climate-focused investing has gone mainstream. Assets under management held in green funds are surging. Total AUM using a climate change or carbon criterion hit $4.18 trillion in 2020, up 39% from 2018, according to US SIF.2 The menu of investment products seeking to address climate concerns has grown in tandem. In 2018, there were fewer than 50 equity funds with an environmental or climate-related purpose or strategy; by 2021, there were more than 400, according to Morningstar. Sustainability-minded investors are increasingly viewing a company’s alignment with 1.5° or 2° as a proxy for a robust environmental strategy, and they are heeding scientists’ calls for action on lowering emissions. A study by State Street Associates published in October 2021 found that there has been a “noticeable decarbonization trend globally” among institutional investor equity portfolios since 2019. And an April 4 report by the U.N.’s Intergovernmental Panel on Climate Change, or IPCC, sounded an alarm that greenhouse gas emissions must peak by 2025 and be reduced by 43% by 2030 if the world is to hit net zero by 2050 and limit warming to 1.5° by 2100. It is this context — the rising momentum behind environmentally conscious investing alongside the growing urgency to address climate change — that makes understanding the current state of equity fund alignment valuable.

1 This study was prepared and finalized before the U.S. Securities and Exchange Commission proposed amendments to its fund “Name Rule” and proposed new ESG disclosure requirements for investment companies on May 25, 2022.

2 US SIF’s total represents asset classes and investment vehicles beyond the equity mutual funds and ETFs used for this analysis.

Limiting the global temperature increase to the Paris Agreement’s goal of roughly 1.5° above preindustrial levels is in theory the primary goal of any net zero or climate change-focused commitment. Even under this ambitious 1.5° scenario, the world still faces significant harm from climate change — coral reefs would decline as much as 90%, up to 14% of terrestrial species would face a very high risk of extinction and 40% of megacities globally would record a heat index higher than 105°F — but the world would stave off much greater losses to nature and human society, according to the IPCC’s February 2022 report on climate adaptation.

Missing the Paris Agreement’s “well below 2°” goal would put 10 million more people at risk from sea level rise and direct flood damage could be twice as high, according to the IPCC’s adaptation report. At 3° of warming, disruption to ports and coastal infrastructure could impact entire financial systems, and risks to agricultural yields are 3x higher than at 2°.

Our analysis shows that 32% of the broad fund universe is poised to meet a 2° warming scenario, while 46% of funds are poised to overshoot even a less ambitious 3° warming scenario. The picture is slightly better for green funds: 39% of green funds are on track to meet a 2° warming scenario.

But 33% of green funds — over 100 funds representing close to $120 billion in market value — are on a trajectory to overshoot 3°. The same proportion of climate-specific funds — 17 out of 51 — are set to overshoot 3°. Fourteen green funds are more than 500 tonnes of CO2e per $1 million invested over budget against a 3° pathway. These funds’ names use terms including “climate change,” “ecological” and “clean technology.”

In terms of market value rather than number of funds, the green funds are somewhat better positioned than the broad universe. A greater share of green fund market value is aligned with 1.5° or 2°, whereas for the broad fund universe, a greater share of market value is aligned with 3° or above 3°. However, in both groups of funds, at least one-third of market value is on a trajectory to overshoot even a 3° scenario. In the narrower set of climate funds, market value is better aligned with 2°, but more than 20% of market value is set to overshoot 3°.

Data as of April 19, 2022.

Analysis uses S&P Global Trucost Paris Alignment data to assess the difference between a company's projected pathway for Scope 1 and Scope 2 greenhouse gas emissions and the required pathway to reach alignment with three different goals from 2012 to 2025. The most ambitious is a goal of limiting warming to "well below" 2°C, or 1.5°C. The second is a goal of limiting warming to 2°C. The third and least ambitious is a goal of limiting warming to 3°C. The broad fund universe represents 11,780 equity funds. The subset of green funds represents 334 funds. The climate funds subset of green funds represents 51 funds.

Design credit: Zain Ullah; Cat weeks

Sources: S&P Global Trucost; S&P Global Sustainable1

Each of the three scenarios in this analysis represents a different emissions budget, which reflects the level of global warming expected in the long term in that scenario. A 3° scenario has a larger emissions budget than a 2° scenario, which has a larger budget than a future limited to 1.5°. As expected, more funds in both the green-identified cohort and the broad fund universe are on track to meet a less ambitious 3° warming scenario. Yet in all three warming scenarios, at least one-third of green funds are over budget.

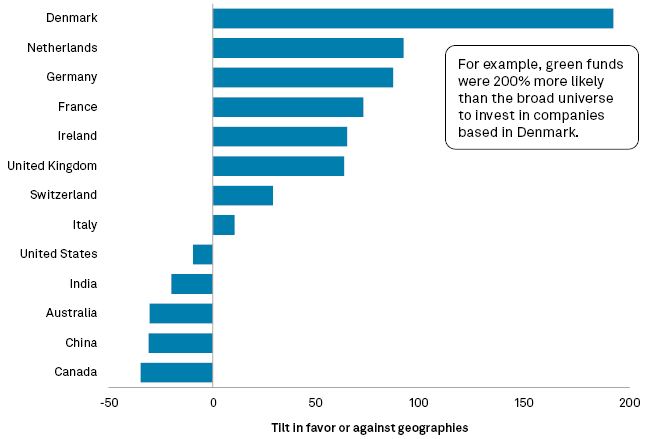

The green funds over budget by the largest amount tend to be more focused on emerging and Asian markets, a finding consistent with the energy use and generation mix of fast-growing, industry-heavy countries. Yet there are also examples among the 10 most under-budget funds that focus on exposure to India and Asia, showing that Paris-aligned holdings are not in short supply in these regions. Green funds in the analysis tend to have more exposure to Europe and less exposure to China, Canada and the U.S. compared to the broad fund universe.

Geographic tilt of 334 green funds versus broad fund universe (%)

Data as of April 19, 2022.

Analysis uses S&P Trucost Paris Alignment data to assess the difference between a company's projected pathway for Scope 1 and Scope 2 greenhouse gas emissions, and the required pathway to reach alignment with three different goals from 2012 to 2025. The most ambitious is a goal of limiting warming to "well below" 2°C, or 1.5°C. The second is a goal of limiting warming to 2°C. the third and least ambitious is a goal of limiting to 3°C.

Sources: S&P Global Trucost; S&P Global Sustainable1

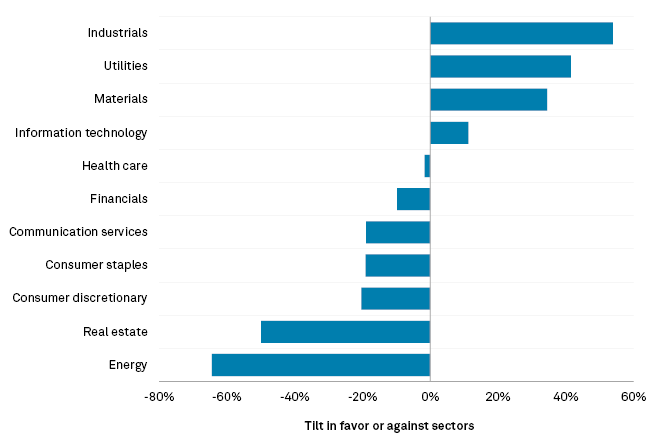

The green funds also tend to be overweight in the technology, materials, utilities and industrials sectors, and less exposed to the energy and real estate sectors, compared with the broad fund universe.

Sector tilt of 334 green funds versus broad fund universe

Data as of April 19, 2022.

Analysis uses S&P Trucost Paris Alignment data to assess the difference between a company's projected pathway for Scope 1 and Scope 2 greenhouse gas emissions, and the required pathway to reach alignment with three different goals from 2012 to 2025. The most ambitious is a goal of limiting warming to "well below" 2°C, or 1.5°C. The second is a goal of limiting warming to 2°C. the third and least ambitious is a goal of limiting to 3°C.

Sources: S&P Global Trucost; S&P Global Sustainable1

While a significant number of green funds are over budget in each scenario, they are generally closer to aligning with their budgets than the broad fund universe. A regression analysis shows that the emissions budget performance of green funds is statistically different from that of the broad fund universe.3 The median green fund is much closer to being on budget in all three temperature scenarios than the broad fund universe. In the 1.5° warming scenario, for example, the median green fund is over budget by 116 tonnes of CO2e per $1 million invested, whereas the median of the broad fund universe is over budget by 212 tonnes of CO2e per $1 million invested — almost twice as much. Both the cohort of green funds and the broader universe are missing the Paris target, but green funds are closer to the mark.

3 See the Appendix for more detail.

Data as of April 19, 2022.

Analysis uses S&P Trucost Paris Alignment data to assess the difference between a company's projected pathway for Scope 1 and Scope 2 greenhouse gas emissions, and the required pathway to reach alignment with three different goals from 2012 to 2025. The most ambitious is a goal of limiting warming to "well below" 2°C, or 1.5°C. The second is a goal of limiting warming to 2°C. the third and least ambitious is a goal of limiting to 3°C. Outlers were excluded from this chart to improve visibility of the distribution.

Sources: S&P Global Trucost; S&P Global Sustainable1

Companies are under pressure to understand their warming trajectory and plan accordingly to decarbonize. This same analysis can be extended to equity and mutual funds, which represent trillions of dollars of investments and play an important role in the energy transition of the broader economy. Our analysis points to a systemic issue — few funds, even those that describe themselves using green or climate-specific language, are on track to meet the goal of the Paris Agreement. Understanding the trajectory is an important step toward planning for a low-carbon future.

While our analysis shows that equity funds have a long journey ahead to meet the goal of the Paris Agreement, many misaligned funds are only slightly over budget: 116 of the over-budget funds in a 1.5° scenario are off by less than 100 tonnes of CO2-equivalent per $1 million invested. By some measures, green funds are closer to alignment than the broad universe of funds. And dozens of funds in our analysis are under budget in all three warming scenarios, showing that Paris alignment is achievable — though alignment appears to be the exception rather than the rule.

This analysis began with the universe of equity mutual funds and exchange-traded funds available on the S&P Capital IQ platform. From this universe, we identified 11,780 funds with a minimum market value of $5 million, with a minimum of 15 holdings, and for which at least 50% of market value is covered by Trucost Paris Alignment data. For the vast majority of funds, coverage is very high: more than 9,000 funds have coverage of 80% or higher.

To create a set of green funds, we searched fund names and descriptions as they appear on S&P Capital IQ for instances of more than 60 keywords or text strings related to renewable energy, sustainability, emissions, climate change and other green terminology in fund names and descriptions. The search results were manually vetted to remove false positives. Some funds in our final universe of 334 green funds do not limit their investments to green or environmentally focused companies.

To create a subset of climate funds, we searched fund names for keywords limited to climate, Paris, transition, carbon and net zero.

Our underlying metric of emissions in this analysis is tonnes of CO2-equivalent above or below a company’s budget, which is its allowable emissions forecasted through 2025 in a given warming scenario. After calculating the budget on a fund basis by apportioning the budgets of its holdings based on their size, we then divide by the fund’s market value, measured in $M. This results in a final metric for this analysis of tonnes of CO2e per $1 million invested.

The above means that emissions attributed to fund f are computed as the sum of the emissions of each of its constituents, weighted by f’s share of ownership in each constituent c, and finally normalized by the fund’s value V(f). The resulting measure is the number of tonnes of CO2e above budget (or below budget, if negative) for each $1 million invested in fund f.

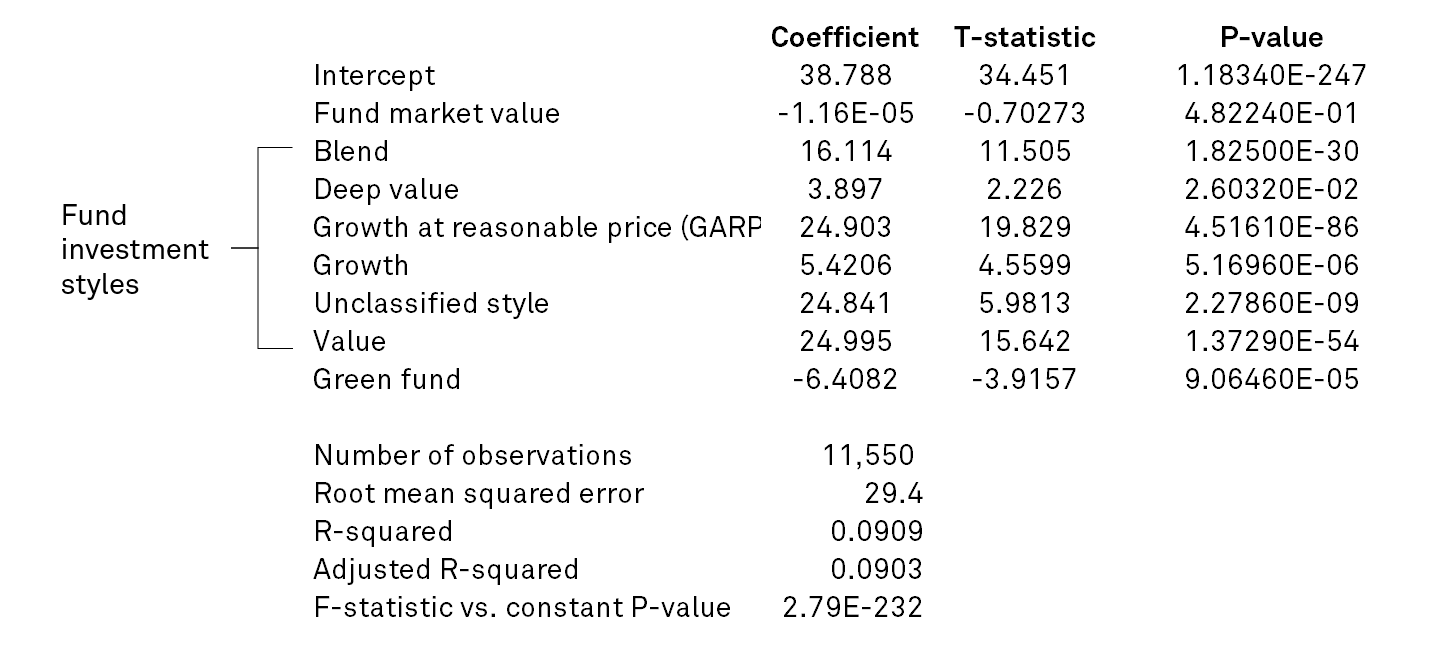

To measure the significance of the difference in emission budget over/under values across the group of green funds and the non-green funds in the broad fund universe, we run the following regression. We find that the variable of whether a fund is in the group of green funds has statistical significance, but also that its significance is similar to another variable: a fund’s investment style.

![]()

We regress the percentile that fund f belongs to scoreQf on a constant variable indicating if the fund is green, on the fund’s market value and on the fund’s style. The results for quantiles computed for the 1.5° temperature scenario, below, are representative of all three scenarios. The fund style “aggressive growth” is used as the baseline.

The green fund variable coefficient is negative and statistically different from 0, suggesting that membership in the green fund group does matter. Notably, most investment style coefficients are larger in absolute value than the green funds’ coefficient, suggesting that the style label is more correlated with emissions than membership in the green funds group. The size of the fund is shown to not be statistically significant.

The tilt used in the sector and geography exposure charts is defined as follows:

![]() is the sum of the value invested into sector or geography s by the green funds (f∈G).

is the sum of the value invested into sector or geography s by the green funds (f∈G).

![]() is the overall value of the green funds, so their ratio is the percentage invested into s by the green funds. The NG figures represent the same quantities for the non-green funds. Therefore, T(s) equals 0 if green and non-green funds as a whole invest the same percentage of their value in sector s. T(s) is smaller than 0 if the green funds as a whole are underweight in s, compared to the non-green funds.

is the overall value of the green funds, so their ratio is the percentage invested into s by the green funds. The NG figures represent the same quantities for the non-green funds. Therefore, T(s) equals 0 if green and non-green funds as a whole invest the same percentage of their value in sector s. T(s) is smaller than 0 if the green funds as a whole are underweight in s, compared to the non-green funds.

Importantly, our analysis only includes Scope 1 emissions, those created by company operations, and Scope 2 emissions, generally those associated with any electricity a company purchases. This analysis does not include Scope 3 indirect emissions, which occur in the supply chain — including when customers use the products or services the companies provide. Scope 3 emissions are disclosed by far fewer companies, and ranges of modelling error are likely wider than in modelling Scope 1 and Scope 2. For this reason, S&P Global excludes Scope 3 from Paris Alignment assessments to limit the chances of mistaken inferences.