Recent and intensifying natural disasters underscore the reality of climate change. In 2021, the Atlantic hurricane season had 21 named storms, including four hurricanes of Category 3 or higher (wind speed of 111+ mph).[1] California again suffered from raging wildfires, with more than 2.6 million acres burned and 3,600 structures destroyed.[2] A new report from the United Nations Intergovernmental Panel on Climate Change (IPCC) warns of major and intensifying risks in the decades to come, particularly between the years 2040 and 2100.[3] More than ever, it is essential to consider what may lie ahead to strategically prepare for rising climate risk.

Financial institutions with mortgage portfolios are especially vulnerable to material potential risks from climate change. The effects of rising seas and hurricanes alone could cost coastal cities USD1tr each year by 2050, according to the Global Commission on Adaptation. But how can institutions quantify these risks and prepare? The Climate Service (“TCS”), now a part of S&P Global, developed the Climanomics® platform to assess climate-related risks under different scenarios to enable mortgage lenders to quantify and compare risks.

Regulators respond to climate risks

Financial market and regulatory bodies around the world are responding to climate change with a range of initiatives to encourage disclosure of related risks. This includes mandating the use of scenario analysis to assess the potential risks of climate change to bank and insurance company portfolio holdings and lending activity. According to the Task Force on Climate-related Financial Disclosures (TCFD),[4] climate scenarios explore alternative pathways for understanding how climate change, climate policy and technology could evolve in the future. While hypothetical, these scenarios provide a global and harmonized reference set of climate trajectories that serve as a starting point for assessing climate risks to the economy and financial system. As such, they are the basis for evaluating strategic and/or financial implications of climate-related risks and opportunities that may significantly alter the basis for business-as-usual assumptions.

Reference scenarios evolve

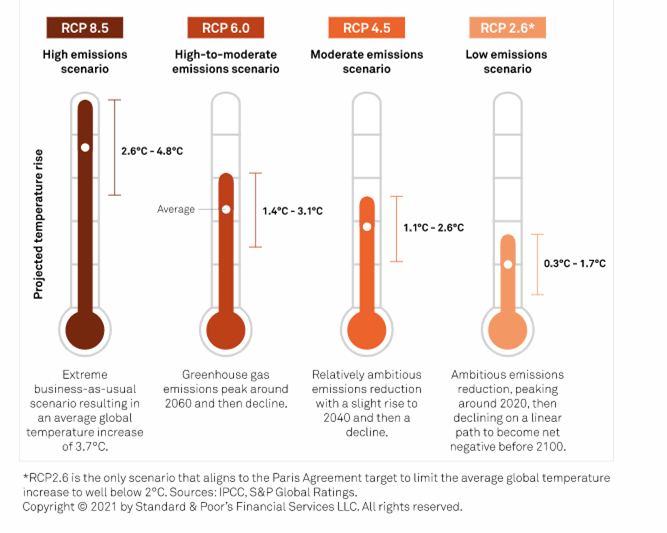

The IPCC published a first set of climate change scenarios in 1992 to provide a common reference point for climate research, responding to the need for standardization of climate data sources and assumptions used in physical climate assessments. For the IPCC’s fifth Assessment Report, integrated assessment modelers, climate modelers, terrestrial ecosystem modelers and emission inventory experts[5] collaborated to define four greenhouse gas (GHG) Representative Concentration Pathways (RCPs) and global warming increase projections ranging from 0.3 to 4.80 C, which form the basis for models portraying distinct climate futures.

Figure 1: The Four RCP Pathways

For assessing climate risk to economies and the financial system, the Network for Greening the Financial System (NGFS), a global network of central bank and financial supervisors, built on the RCP framework to define common reference scenarios that more explicitly consider the transition and strength of response. These are based on representative scenarios that consider orderly and disorderly transitions, as well as the failure to meet climate goals due to inaction or inadequate action. In its sixth Assessment released in 2021-22, the IPCC explicitly incorporated socioeconomic trajectories to its projections of climate futures, adding a highly optimistic scenario where global CO2 emissions are cut to net zero around 2050. It is likely that the NGFS will evaluate its current scenarios to incorporate the new IPCC enhancements.

Scenarios Shed Light on Mortgage Exposures

The Climanomics platform assesses climate-related risks under the four RCP scenarios, which can be easily aligned with the NGFS scenarios, enabling mortgage lenders to quantify and compare risks. This includes evaluating the potential impacts of seven physical hazards on each asset in a portfolio for each decade to 2100, including: extreme temperatures, drought, coastal flooding, fluvial flooding, water stress, tropical cyclones and wildfires. Viewing risks over decades reveals whether losses are likely to increase gradually or experience future spikes. And, by viewing portfolio losses by hazard type, mortgage lenders can better monitor and manage hazard-specific risks and mitigations.

Assessments of hazards and vulnerabilities are considered together for each asset to estimate the average annual loss associated with climate risk, enabling mortgage lenders to evaluate the vulnerability of their portfolios at a granular level. In addition, an institution can stress test its mortgage portfolio by modeling and aggregating the financial impact of all climate-driven losses for individual properties and capturing the potential increase in the likelihood of individual mortgage defaults. So, by reporting the losses attributed to climate change and the nature of the losses (e.g., increased cooling costs or foundation damage), it is possible to interpret the losses and consider them within existing credit assessment frameworks.

Taking Action

Scenario analysis, enabled by the Climanomics platform, provides an important lens through which to evaluate the impact of climate-related events on mortgage portfolios. It is an extremely useful tool to compare exposure by region and by hazard type, and to pinpoint areas of risk for assessing needed insurance coverage and appropriate mitigation and adaptation strategies. It is also clear that regulatory requirements for climate analysis are beginning to change in the U.S., given the Securities and Exchange Commission’s March 2022 proposal to enhance and standardize climate-related disclosures for publicly traded companies. Taking action now to be prepared for scenario analysis and stress testing can help mortgage lenders get ahead of the curve.

Click here for more information on TCS’s Climanomics solution.

[2] Cal Fire Incident Archive, www.fire.ca.gov/incidents/2021/.

[5] "The representative concentration pathways: an overview”, August 2, 2011, https://psl.noaa.gov/ipcc/cmip5/rcp.pdf.