Engineering and Construction Materials and Equipment Costs Fall for First Time Since November 2020 while Subcontractor Labor Costs Continue to Rise

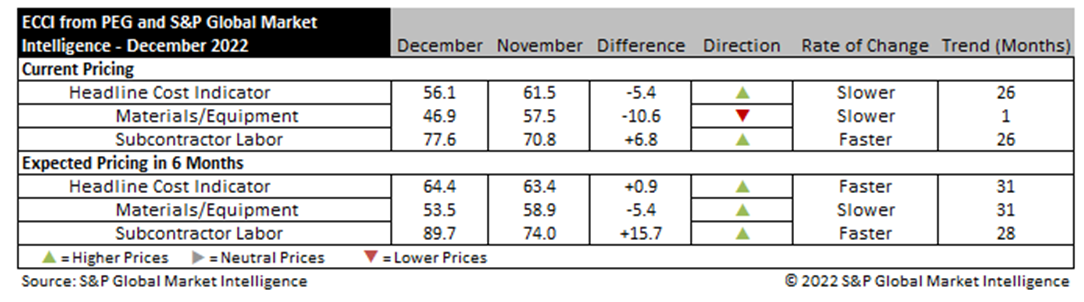

WASHINGTON, D.C. – January 9, 2023 – Engineering and construction costs increased again in December, according to the Engineering and Construction Cost Indicator from PEG and S&P Global Market Intelligence. The headline Engineering and Construction Cost Indicator, a leading indicator measuring wage and material inflation for the engineering, procurement and construction sector, declined to a level of 56.1 from 61.5 in November, indicating price increases in December were less widespread. Although the headline indicator has recorded increasing prices for 26 months, the sub-indicator for materials and equipment costs slid 10.6 points to 46.9, the first sub-50 result in two years. The subcontractor labor indicator rose to 77.6, adding 6.8 points in December, keeping the headline indicator in expansionary territory.

The equipment and materials indicator’s drop below the breakeven point of 50 ended 24 consecutive months of price growth. Readings for ten of the 12 components dropped, with the three steel categories and copper-based wire and cable joining the two freight rates in contractionary territory. Weak demand has undercut steel pricing, with the well-supplied market shifting leverage to buyers in recent months. Meanwhile, soft global trade activity continues to push ocean freight prices lower. The transformers and electrical equipment components remain quite high, however, with supply chain issues and long backlogs maintaining a tight market.

The sub-indicator for current subcontractor labor costs came in at 77.6 in December, up from November’s 70.8. According to survey responses, labor costs continued to rise in all regions of the United States and Canada. This indicator has not seen values below 70.0 since October 2021.

“Labor costs will remain supported, even as activity in commercial and residential construction slows,” said Emily Crowley, Associate Director of Economics S&P Global Market Intelligence. “The construction industry is still struggling with widespread labor shortages which has kept firms hiring even as business slows. Construction in the heavy and civil engineering sector will be a bright spot in 2023, supported by projects linked to the Infrastructure Investment and Jobs Act and the Inflation Reduction Act. Additional activity from the energy sector will also compete for labor. Demand from these projects will keep occupations like welders, electricians and equipment operators in high demand, keeping wages supported through the end of 2023.”

The six-month headline expectations for future construction costs indicator increased slightly, to a reading of 64.4 in December. The six-month expectations indicator for materials and equipment came in at 53.5, 5.4 points lower than last month’s figure. Additionally, the three steel categories joined the two ocean freight rates in sub-50 territory, indicating survey respondents expected lower pricing in six months. The six-month outlook readings declined to exactly 50 for shell and tube heat exchangers, ANSI pumps and compressors, and gas/steam turbines, suggesting expectations are for flat pricing through the near term. The six-month expectations indicator for sub-contractor labor jumped 15.7 points to 89.7, indicating nearly all survey respondents expect higher labor costs in six months; the subcontractor indicator for every region increased.

Respondents continued to report material shortages in December, particularly for electronic components, electrical equipment, and labor.

To learn more about the Engineering and Construction Cost Indicator or to obtain the latest published insight, please click here.

# # #

About S&P Global Market Intelligence

At S&P Global Market Intelligence, we understand the importance of accurate, deep and insightful information. Our team of experts delivers unrivaled insights and leading data and technology solutions, partnering with customers to expand their perspective, operate with confidence, and make decisions with conviction.

S&P Global Market Intelligence is a division of S&P Global (NYSE: SPGI). S&P Global is the world’s foremost provider of credit ratings, benchmarks, analytics, and workflow solutions in the global capital, commodity, and automotive markets. With every one of our offerings, we help many of the world’s leading organizations navigate the economic landscape so they can plan for tomorrow, and today. For more information, visit www.spglobal.com/marketintelligence.

Media Contact:

Kate Smith, S&P Global Market Intelligence

P. +1 781 301 9311

E. katherine.smith@spglobal.com