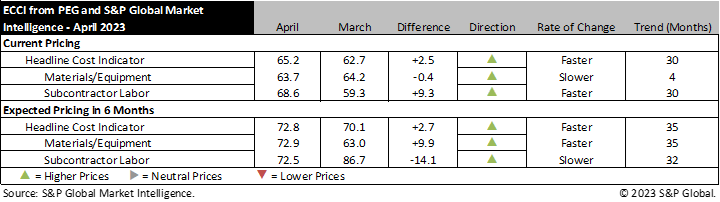

WASHINGTON, D.C. – April 26, 2023 – Engineering and construction costs increased again in April, according to the Engineering and Construction Cost Indicator from PEG and S&P Global Market Intelligence. The headline Engineering and Construction Cost Indicator, a leading indicator measuring wage and material inflation for the engineering, procurement and construction sector, rose to 65.2 this month from 62.7 in March, indicating price increases were slightly more widespread than last month. The sub-indicator for materials and equipment costs fell to 63.7 this month from 64.2 in March; price increases have remained strong since the December sub-50 reading. The sub-indicator for subcontractor labor costs increased to 68.6 this month, up from 59.3 in March.

The equipment and materials price indicator continued to indicate rising prices, with 10 of the 12 components posting increases. The two freight categories returned to contractionary territory in April after being near neutral in March. Carbon steel pipe increased to 63.6 this month, indicating prices are on the rise after nine months of steady declines. Meanwhile, soft global trade activity continues to push ocean freight prices lower. Transformers and electrical equipment components remain high, with supply chain issues and long backlogs maintaining a tight market. The copper-based wire and cable indicator increased 10 points to 80.0 this month, the second straight month of double-digit increases.

“Copper wire and cable prices continue to find support from elevated copper prices and tight overall supply conditions as growth in demand has outpaced available supply in recent years,” said Amanda Eglinton, Economics Associate Director, S&P Global Market Intelligence. “Rising domestic production in response to elevated profit margins for wire producers combined with higher copper wire imports, falling copper prices and slowing demand from the residential sector will provide price relief by the second half of the year.”

After falling under 70.0 for the first time since 2021 last month, the sub-indicator for current subcontractor labor costs increased to 68.6 this month, closer to the values seen during the last six months. According to survey responses, labor costs continued to rise in all regions of the United States and Canada.

The six-month headline expectations for future construction costs indicator increased by 2.7 points to a reading of 72.8 in April. The six-month expectations indicator for materials and equipment came in at 72.9, 9.9 points higher than last month’s figure. The outlook for steel looks much stronger than last month with each of the three categories registering increases of around 20 points in April, leaving the average value for steel slightly over 70.0.

The six-month expectations indicator for sub-contractor labor registered 72.5, down significantly from last month’s reading of 86.7. Nonetheless, a majority of survey respondents expect higher labor costs in six months. The U.S. Northeast and West continue to show strong expectations for labor growth. In contrast, labor cost expectations softened in the U.S. Midwest and South, and in the Eastern and Western regions of Canada.

Respondents continued to report material shortages in April, particularly for transformers, electrical equipment, and labor.

To learn more about the Engineering and Construction Cost Indicator or to obtain the latest published insight, please click here.

# # #

About S&P Global Market Intelligence

At S&P Global Market Intelligence, we understand the importance of accurate, deep and insightful information. Our team of experts delivers unrivaled insights and leading data and technology solutions, partnering with customers to expand their perspective, operate with confidence, and make decisions with conviction.

S&P Global Market Intelligence is a division of S&P Global (NYSE: SPGI). S&P Global is the world’s foremost provider of credit ratings, benchmarks, analytics and workflow solutions in the global capital, commodity, and automotive markets. With every one of our offerings, we help many of the world’s leading organizations navigate the economic landscape so they can plan for tomorrow, today. For more information, visit www.spglobal.com/marketintelligence.

Media Contact:

Kate Smith, S&P Global Market Intelligence

P. +1 781 301 9311

E. katherine.smith@spglobal.com