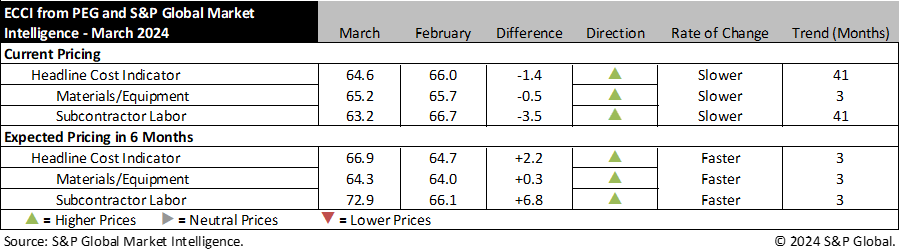

New York – March 27, 2024 – Engineering and construction costs increased again in March, according to the Engineering and Construction Cost Indicator from PEG and S&P Global Market Intelligence. The headline Engineering and Construction Cost Indicator, a leading indicator measuring wage and material inflation for the engineering, procurement and construction sector decreased 1.4 points to 64.6 this month, indicating price increases are slightly less widespread than in February. The sub-indicator for materials and equipment costs edged down 0.5 points to 65.2 while the sub-indicator for subcontractor labor costs fell to 63.2 in March from 66.7 last month.

The equipment and materials indicator continued to show rising prices in March. Only four of the 12 components increased compared to last month with an additional two remaining flat. Two categories are below 50; fabricated structural steel saw a moderate decline to join carbon steel pipe in contractionary territory with a reading of 45.0, while alloy steel pipe and shell and tube heat exchangers both settled at neutral readings of 50.0. The largest growth was seen in the transformers category which increased 13.6 points to a reading of 81.8, the same value as electrical equipment. Ocean freight categories saw a slight reprieve after two months of significant increases, settling slightly lower at 86.4 for Asia to U.S. routes and 90.0 for Europe to U.S. The remaining categories saw a variety of movements, but all settled to readings between 55.0-65.0, indicating prices continue to increase for equipment and building materials.

The sub-indicator for current subcontractor labor costs saw a modest 3.5-point decrease compared to last month. Many regions and employment categories saw decreases across the U.S.—especially in the West region—but this was partially offset by increases in Canada, resulting in only slightly looser pricing conditions. About half of the subcontractor labor categories are in neutral territory in the U.S. this month with the others ranging between 62.5-75.0, while all of Canada registered values of 66.7. After one month of very strong increases, labor tightness in the U.S. West region appeared to soften this month with significant declines registered for all employment categories.

"Construction activity continues to surprise to the upside while other areas of the U.S. economy are slowing,” said Emily Crowley, Economics Director, S&P Global Market Intelligence. “Employment gains in heavy and civil engineering accelerated over the second half of 2023 and promise to remain strong over 2024, supported by projects linked to the Infrastructure Investment and Jobs Act, Inflation Reduction Act, and Chips and Science Act. Job vacancies in the construction industry are once again moving higher as hiring outpaces available supply, suggesting continued support for above-average wage gains despite moderating inflation.”

The six-month headline expectations for future construction costs indicator increased modestly to 66.9 in March, the third straight increase after the single month of expected price declines recorded in December. The six-month expectations indicator for materials and equipment came in at 64.3, just 0.3 points higher than last month’s figure. Five of 12 categories saw price expectations increase this month, five saw declines and two remained unchanged. Fabricated structural steel saw an 8.3-point decrease to join carbon steel pipe at a neutral reading of 50.0. Meanwhile, respondents expect higher prices in six months for all other materials, with especially high readings for transformers and electrical equipment, which recorded readings of 80.0 and 77.3 respectively.

The six-month expectations indicator for sub-contractor labor saw a 6.8-point increase to a reading of 72.9, returning to a level more consistent with readings over the last twelve months. Modest increases occurred in almost all regions and employment categories except for the U.S. Midwest which saw moderate declines and a return to a neutral environment. Within the U.S., the tightest labor market conditions exist in the South and West regions where the indicators strongly expect higher prices in the six months.

Respondents reported some shortages again this month for electrical equipment and labor, especially in the Gulf Coast area as seasonal projects get up and running for the year. Shortages were also reported for labor of all types, particularly along the Gulf Coast. Survey respondents also indicated that ocean freight rates continue to remain higher due to shipping concerns in the Red Sea and delays at the Panama Canal.

To learn more about the Engineering and Construction Cost Indicator or to obtain the latest published insight, please click here.

# # #

About S&P Global Market Intelligence

At S&P Global Market Intelligence, we understand the importance of accurate, deep and insightful information. Our team of experts delivers unrivaled insights and leading data and technology solutions, partnering with customers to expand their perspective, operate with confidence, and make decisions with conviction.

S&P Global Market Intelligence is a division of S&P Global (NYSE: SPGI). S&P Global is the world’s foremost provider of credit ratings, benchmarks, analytics and workflow solutions in the global capital, commodity, and automotive markets. With every one of our offerings, we help many of the world’s leading organizations navigate the economic landscape so they can plan for tomorrow, today. For more information, visit www.spglobal.com/marketintelligence.

Media Contact

Kate Smith, S&P Global Market Intelligence

P. +1 781 301 9311

E. katherine.smith@spglobal.com