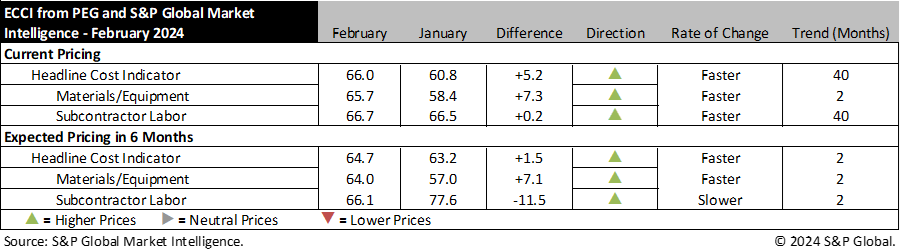

New York – February 28, 2024 – Engineering and construction costs increased again in February, according to the Engineering and Construction Cost Indicator from PEG and S&P Global Market Intelligence. The headline Engineering and Construction Cost Indicator, a leading indicator measuring wage and material inflation for the engineering, procurement and construction sector increased 5.2 points to 66.0 this month, the second moderate step up after the exceptionally weak reading in December. The sub-indicator for materials and equipment costs climbed 7.3 points to 65.7 while the sub-indicator for subcontractor labor costs edged up to 66.7 in February from 66.5 last month.

The equipment and materials indicator continued to show rising prices in February. Readings for eight of the 12 components increased compared to last month and only two remain below 50; carbon steel pipe and alloy steel pipe remain in contractionary territory with readings of 41.7 and 45.0, respectively. The largest growth was seen in the ocean freight categories which saw a second straight month of significant increases. In February, ocean freight – Asia to U.S. sits at 95.0 and Europe to U.S. is at 100.0. ANSI pumps and compressors, gas and steam turbines and transformers each saw declines this month, but all remain solidly in expansionary territory with values between 61.1 and 68.2. Outside of ocean freight, the highest reading for February was for electrical equipment which saw another increase and remains very tight at 81.8.

“Prices for electrical motors and transformers continue to be elevated, primarily due to a persistent shortage in electrical steel supply; prices are not expected to decrease significantly throughout the year. Lead times continue to increase, with large transformers at the four-year mark. The market has reached a saturation point, preventing any drastic price escalations,” said Philip Azar, Senior Economist, S&P Global Market Intelligence. “In contrast, the prices for circuit breakers and switch gears, which do not depend on electrical steel, are expected to experience a softer pricing environment. This is attributed to a stable supply of copper and a decrease in demand from the residential construction sector, leading to a gradual easing of prices.”

The sub-indicator for current subcontractor labor costs saw a very minor 0.2-point increase compared to last month. Many regions and employment categories saw increases across the U.S.—especially in the West region—but this was partially offset by declines in Canada, resulting in only slightly tighter pricing conditions. All subcontractor labor categories remain in growth this month in the U.S., but Eastern Canada has returned to neutral territory in February. The West and South U.S. regions and Western Canada have the highest indicator values, with most readings between 62.5 and 87.5, with Instrumentation and Electrical subcontractors in the U.S. West recording a value of 100.0.

The six-month headline expectations for future construction costs indicator increased modestly to 64.7 in February, the second straight increase after the single month of expected price declines recorded in December. The six-month expectations indicator for materials and equipment came in at 64.0, 7.1 points higher than last month’s figure. Ten of 12 categories saw price expectations increase this month; electrical equipment saw the only decrease and gas and steam turbines remained unchanged. The largest increases occurred for fabricated structural steel and alloy steel pipe, 16.7 and 15.0 points respectively, moving each noticeably above the neutral mark of 50 after weaker expectations last month. Carbon steel pipe and shell and tube heat exchangers saw neutral readings of 50.0 this month, and all other categories are in expansionary territory, indicating expectations for higher prices in six months.

The six-month expectations indicator for sub-contractor labor saw a 11.5-point decrease to a reading of 66.1, settling to a more moderate reading after large swings the last two months. Significant decreases occurred in all regions and employment categories in the U.S., but all categories still expect higher costs in six months with readings between 57.1 and 72.2. Readings are even tighter in Canada where values fall between 66.7 and 87.5, with the tightest expectations in Western Canada.

Respondents reported some shortages again this month for electrical equipment, ready-mix concrete and aggregates. Shortages were also reported for labor of all types, particularly along the Gulf Coast. Survey respondents also indicated that ocean freight rates are higher due to shipping concerns in the Red Sea and delays at the Panama Canal.

To learn more about the Engineering and Construction Cost Indicator or to obtain the latest published insight, please click here.

###

About S&P Global Market Intelligence

At S&P Global Market Intelligence, we understand the importance of accurate, deep and insightful information. Our team of experts delivers unrivaled insights and leading data and technology solutions, partnering with customers to expand their perspective, operate with confidence, and make decisions with conviction.

S&P Global Market Intelligence is a division of S&P Global (NYSE: SPGI). S&P Global is the world’s foremost provider of credit ratings, benchmarks, analytics and workflow solutions in the global capital, commodity, and automotive markets. With every one of our offerings, we help many of the world’s leading organizations navigate the economic landscape so they can plan for tomorrow, today. For more information, visit www.spglobal.com/marketintelligence.

Media Contact:

Katherine Smith, S&P Global Market Intelligence

P. +1 781 301 9311

E. katherine.smith@spglobal.com