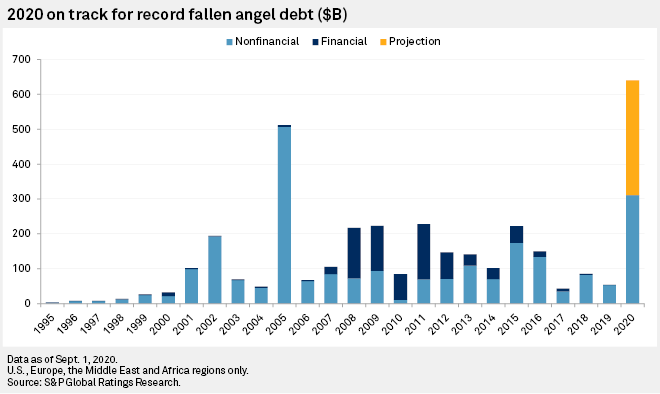

Global fallen angel debt — bonds that have been downgraded to sub-investment grade — is on track to reach an all-time high of $640 billion in 2020, having already amounted to $323 billion in the first six months of the year, according to S&P Global Ratings.

The previous record was $487.86 billion in 2005.

As was the case in 2005, the 2020 total of fallen angel debt — already the second-highest by value on record — was elevated by a downgrade of Ford Motor Co. As the American carmaker slipped back into the sub-investment grade universe once more on March 25, it took $113.86 billion of rated debt with it.

Unlike 2005, when there were only 22 fallen angels in the entire year, 2020 is also historically high in the number of companies downgraded from investment grade to sub-investment grade. At 34, 2020 is already the third-highest annual total on record, chasing the 2009 mark of 57 as the financial crisis bit.

|

The majority of the downgrades have occurred in the U.S. and Europe, the Middle East and Africa, which have experienced downgrade rates of triple-B rated debt — the lowest branch of debt considered investment grade — of 4.7% and 6.9% respectively, whereas there were only four fallen angels from Latin America and one from Asia-Pacific.

The first seven fallen angels of 2020 occurred in January and February and were unrelated to the coronavirus. They included companies such as The Kraft Heinz Co., so far the only consumer products fallen angel this year, and retailer Macy's Inc.

With the arrival of the coronavirus in the U.S. and mandated social distancing, between March 23 and April 20, 17 further companies were downgraded, with automotive and oil and gas companies being particularly hard hit.

In the following wave of downgrades, transportation companies — including three in the airlines subsector — suffered the most.

Debt issuance booms

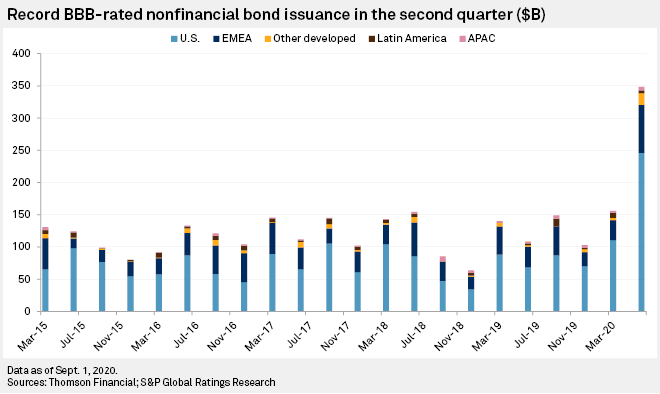

Debt issuance has ballooned this year even as creditworthiness declined, as companies raced to increase their cash buffers.

Issuance of non-financial triple-B rated debt reached record high levels both in the U.S. and EMEA in the second quarter of 2020. At $246 billion, the U.S. total was up from $110.76 billion in the first quarter, while EMEA issuance rose to $74.54 billion from $30.92 billion.

|

The increase in the amount of speculative grade debt issuance was not enough to reverse a decline in the yield of U.S. high-yield corporate debt.

"Thus far the speculative-grade bond market appears to have comfortably absorbed debt that was recently downgraded from triple-B, though most bonds from recent fallen angels have been trading at relatively high levels compared with the speculative-grade composite," Nick Kraemer, head of S&P Global Ratings Performance Analytics, wrote in its report.

The ICE Bank of America U.S. high-yield index option-adjusted spread rose from 357 basis points on Feb. 19 to a peak of 1,087 bps on March 23 as the pandemic took hold in the U.S., before falling back down to 502 bps as of Aug. 31.

The market was supported by announcements from both the Federal Reserve and the European Central Bank that corporate bonds would be included in their respective liquidity support programs, while a large portion of the fallen angel debt is attributable to just a handful of issuers.

The Fed announced its $2.3 trillion in liquidity facilities on March 23. On April 9, the Fed adjusted its primary and secondary corporate bond facilities to include recent fallen angel debt, which coincides with a second bump up in all three asset class series.

"Credit quality has been strained during the COVID-19 pandemic, but liquidity has been abundant as a result of central bank liquidity facilities. Specifically, the Fed's primary and secondary corporate bond purchase facilities were altered to accept the debt of recent fallen angles, which arguably has helped produce a historical high for quarterly triple-B nonfinancial bond issuance in the second quarter," Kraemer wrote.