|

| Evergrande Plaza in Chengdu, China. The negative sentiment flowing from China's property market, exemplified by China Evergrande's woes, is expected to impact steel markets in 2022. |

Missed debt payments by property development giant China Evergrande Group will likely kick off a rough 2022 for the steel industry.

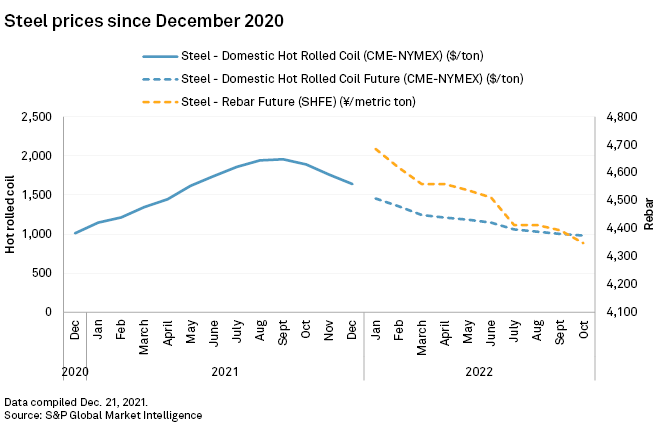

Efforts by the Chinese government to deleverage its highly indebted property sector in 2021 sent Evergrande, its second-largest developer, into a spiral of default, and many of its peers may soon face similar challenges. That means hard times for steelmakers: On the Shanghai Futures Exchange, steel rebar, mainly used for construction projects, traded

Beijing has had a change of heart in recent months, offering policy supports to property developers such as Evergrande, but analysts fear the moves are inadequate and more defaults are still to come.

Evergrande's crisis is "just the tip of the iceberg," according to Stuart Burns, founder and editor-at-large of MetalMiner.

"Firms like Evergrande are off-loading stock to meet interest payments, depressing prices, and the resulting fall in residential property prices is dissuading new construction," Burns said in an interview. "A depressed construction sector [in China] will weigh on iron ore, steel and aluminum prices in 2022, extending the depressing effect it has already had in the fourth quarter."

Growth in China, the world's second-largest economy, has been slowing for two quarters amid concerns about a deflating property bubble and Evergrande's debt crisis. The property downturn is projected to continue through 2022. S&P Global Ratings expects to see more defaults in 2022 and as much as one-third of Chinese developers to be under liquidity pressure. It also forecasts that China residential sales will fall by 10% in 2022 and further decline by 5% to 10% in 2023, with property prices to fall by up to 3%.

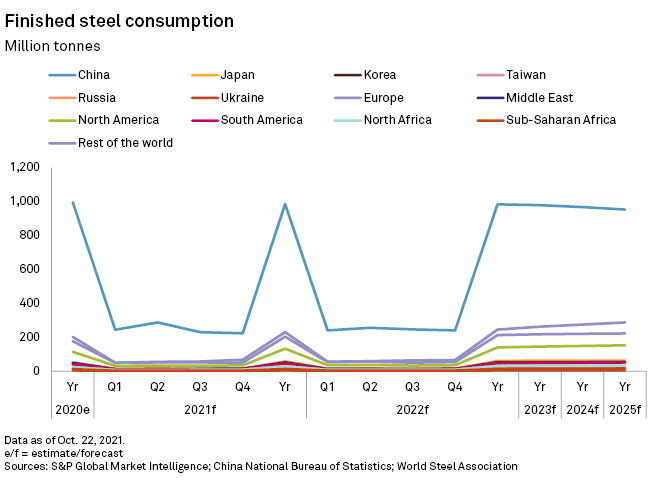

None of that is good news for steel producers. China's steel demand is expected to fall 0.7% to 947 million tons in 2022, following a 4.7% decline in 2021, dragged down by weakening property sector and COVID-19 uncertainties, Reuters reported Dec. 15, citing government-backed think tank China Metallurgical Industry Planning and Research Institute, or MPI.

Investors' 2022 outlook remains bearish, as the steel rebar futures for November and December 2022 were trading below 4,250 Chinese yuan/t on Dec. 17, below the spot price that same day.

Bigger picture

But the steel industry has more issues than the financial woes of its largest buyers. There is a "much bigger picture" impacting China's market, said Westpac Senior Economist Justin Smirk, including decarbonization efforts and the government's attempts to moderate growth as part of its commitment to net-zero emissions by 2060.

In April, the government cracked down on mills in the country's largest steelmaking province, ordering curtailments in nearly all the mills to reduce smog and carbon emissions. The government is pushing its mills to move to more expensive, lower carbon equipment and processes, and it is closing smaller, inefficient steel mills in favor of larger, more efficient mills.

Production changes combined with the shifts in property development will lead to a "leveling out of steel production in China," Smirk said.

The fall in Chinese steel production this year has already sent iron ore prices tumbling from a record high in May to an 18-month low in November. To achieve the decarbonization goal, MPI expects China's crude steel output to drop

The steel sector also has been under stress since September due to the power crunch, Helen Qiao, head of Asia economics and chief China economist at Bank of America Global Research, said at a Dec. 9 market outlook webinar.

Energy cuts sent China's daily steel output to a 44-month low at 2.3 Mt in October, though it has started to recover, with a 1.2% monthly increase in November. S&P Global Platts expects the upward trend to continue in December as China boosts coal production to ease the power shortage. Steelmakers completed 2021 output cut requirements last month.

Meanwhile, the slowing growth of the manufacturing sector is also expected to weigh on steel demand in 2022, Bruce Pang, head of macro strategy research for China Renaissance Securities, said in an interview.

Market Intelligence forecasts Chinese steel production to remain subdued until after the Beijing Winter Olympics in February 2022. The government is expected to give priority to winter heating needs over industrial energy usage in the months ahead.

The Chinese government appears to be aware of the danger to its property development sector, and it has been willing to offer modest policy assistance that could boost steel.

The government vowed at the Central Economic Work Conference in Beijing to "promote a virtuous circle and healthy development of the real estate industry," according to a Dec. 10 report from the official Xinhua News Agency. China also cut its reserve requirement ratio in early December, a boon to developers seeking loans.

With these policy levers in play, CITIC Futures analysts believe steel demand from the property sector has "begun to edge out of the darkest period," and is expected to see a "marginal recovery" in the first half of 2022, they said in a Dec. 1 note. S&P Global Market Intelligence expects the credit boost will lift steel demand in the construction and manufacturing sectors in the first half of 2022, though prices are expected to continue to decline.

However, there was no big turnaround in property policies, Pang said. The property market has been slowly bidding farewell to the high-debt, high-growth model that China has been used to, he said.

Bank of America's Qiao expects policymakers to do more to support property demand and stabilize overall property developer financing given its importance to China's GDP.

The current stimulus is still "far from being enough," Qiao said.

As of Dec. 31, US$1 was equivalent to 6.35 Chinese yuan.