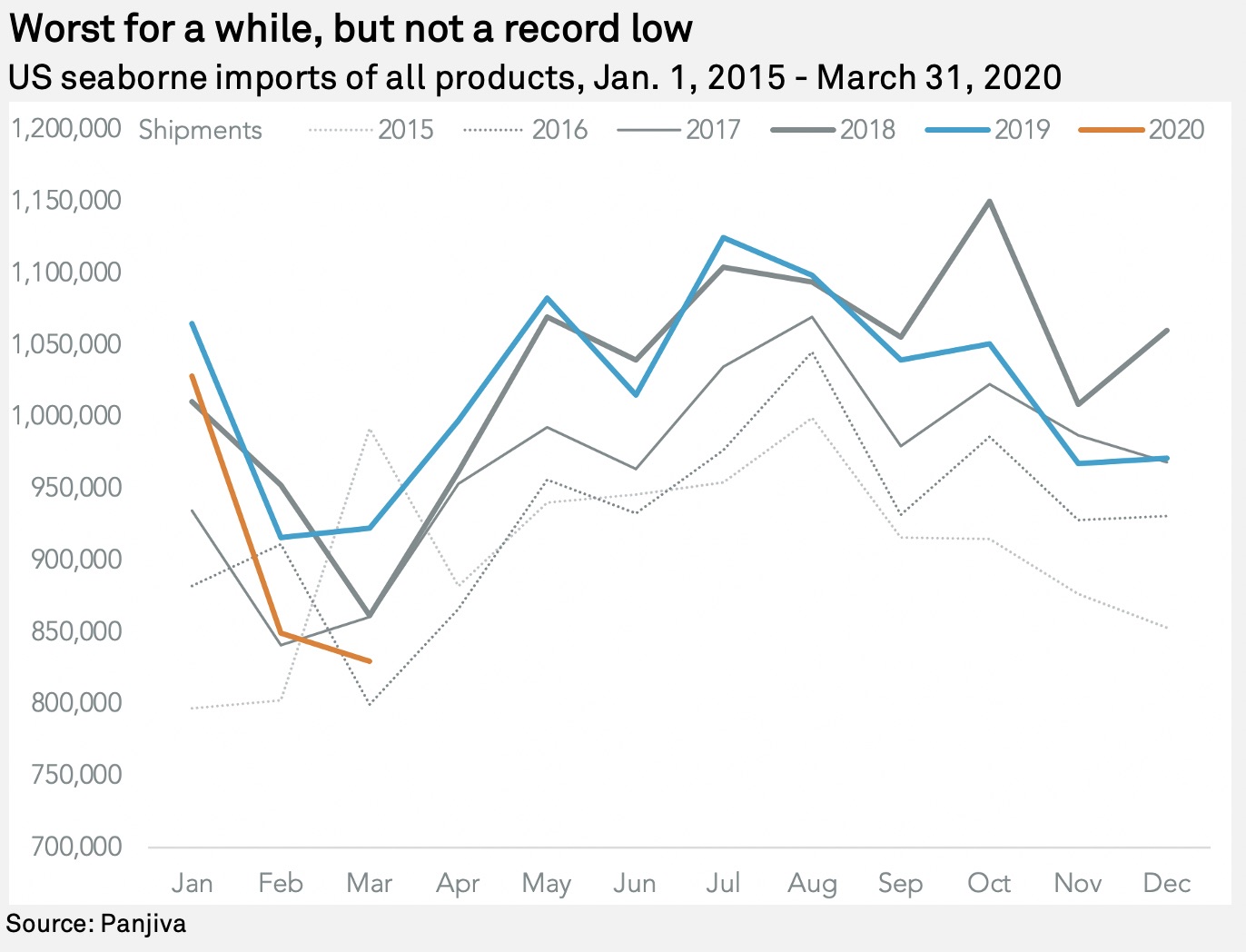

The toll of the new coronavirus disruptions to global trade were clearly visible in U.S. seaborne imports in March, though not perhaps by as much as midmonth data suggested. Panjiva's data shows shipments from all origins fell by 10.1% year over year in March, compared to 15.0% at midmonth as discussed in Panjiva's March 25 research.

Nonetheless, March still saw the fewest number of shipments for a month since 2016. Containerized imports did slightly better with a 9.2% decline and reached their lowest level since February 2017.

|

The intramonth reduction in the rate of decline in imports was largely down to shipments from China, which fell by a still considerable 34.0% year over year to their lowest level since at least 2007 as the full impact of the industrial lockdown made itself felt.

Among other major suppliers, the only significant growth was in shipments from Vietnam, which rose by 35.4%. Yet, as discussed in Panjiva's research of Feb. 21, a shortage of materials from China may lead to a dip in exports from Vietnam to the U.S. for arrivals during April. A degree of that effect may already be visible in imports from other Asian countries with shipments from Asia excluding China in total up by just 2.7%.

Shipments from Europe managed to increase modestly, with a 0.3% rise ending a three-month run of declines. However, the widening lockdowns throughout March will likely trim April arrivals.

Another drag to activity will come from reduced demand for products as well as disruptions to supply chains. Indeed, nearly two-thirds of respondents to a poll at a recent S&P Global webinar indicated that a loss of demand will prove more harmful to corporate earnings in the coming months, ahead of supplier disruptions and logistics problems.

The drag to imports of consumer durables shown by a 21.0% year-over-year drop in imports of furniture and a 17.9% slide in apparel continues earlier declines and may need to fall further given widespread retail outlet closures. Among industrial supplies there was a 16.3% slide in imports of iron/steel — also not helped by widespread tariffs as well as a loss of autos industry demand — while shipments of chemicals declined by just 4.5%.

Among electronics and electricals, which fell by 15.7% year over year as a group, there were particularly notable downturns in washing machines, where imports fell by 72.4% due to the earlier implementation of tariffs; a 49.2% slide in shipments of TVs and monitors, the latter despite increased work-from-home demand; and a 49.1% slide in imports of valve systems which sit at the heart of many capital goods supply chains.

|

Christopher Rogers is a senior researcher at Panjiva, which is a business line of S&P Global Market Intelligence, a division of S&P Global Inc. This content does not constitute investment advice, and the views and opinions expressed in this piece are those of the author and do not necessarily represent the views of S&P Global Market Intelligence. Links are current at the time of publication. S&P Global Market Intelligence is not responsible if those links are unavailable later.