Licensed and regulated financial institutions are essential partners for financial technology companies that seek to offer the broadest and most robust range of financial services to their customers. In the US, this runs the gamut from issuing cards and opening bank accounts to holding deposits and accessing a Federal Reserve account. Banks that enable these services on behalf of fintechs are generally invisible to fintech providers' end users, operating quietly behind the scenes. In this report, we discuss the trend of fintech partner banks and the different approaches emerging in the marketplace.

Banks play a critical role in enabling fintechs to offer financial services to their end customers. For financial institutions, benefits in these partnerships can be found in cost-efficient deposit and revenue growth, but they must reconcile this with the lack of a relationship with the end customer. A variety of approaches are emerging to enable bank-fintech collaborations. Some banks are leaning into banking-as-a-service platform vendors to streamline fintech integrations while others are spinning up their own in-house banking-as-a-service divisions or subsidiaries. Regardless of the approach, strong due diligence, risk management and oversight must be at the forefront of any banking-as-a-service strategy to ensure fintechs are operating in a safe and compliant manner.

Context

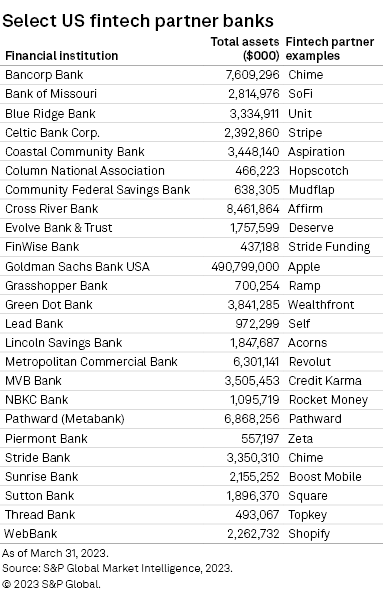

In the US, there are more than 50 financial institutions that support fintechs on an as-a-service basis (i.e., banking-as-a-service). These are commonly referred to as "partner banks" or "sponsor banks" and often have less than $10 billion in assets. Banks of this asset size are exempt from the Durbin Amendment's debit card interchange fee caps, making them particularly attractive to fintechs in that they can help fintechs earn higher margins on debit transactions. Below, we highlight 25 examples of fintech partner banks in the US.

Although it is still early, banking as a service is increasingly top of mind for financial institutions, with the term mentioned on 62 bank earnings calls in 2022, up from six in 2019, according to S&P Global Market Intelligence data. The benefit for banks participating in banking-as-a-service models is increasing deposits and revenue (interchange, interest) at a relatively low cost (no customer acquisition cost). In an analysis of 42 community banks that offer banking as a service, S&P Global Market Intelligence found that these institutions increased deposits 18% on average between the first quarter of 2022 and the first quarter of 2023, whereas deposit growth among other US banks with less than $10 billion in assets was essentially flat during the same period.

Building a banking-as-a-service business means coming to terms with having no direct customer relationship and therefore no means of driving cross-sells or loyalty. Comfort with this understandably varies across the industry. As PNC Financial Services Group Inc. CEO Bill Demchak said on the bank's first-quarter 2021 earnings call, "As the low-cost provider to somebody else who owns the relationship, you've just sold your soul to the devil. ... [W]e need to own the customer relationship, and we need to deserve to own the customer relationship through an offering that doesn't need that fintech platform on the front end."

Reaffirming its position, PNC shut down BBVA Open Platform in 2022 following its acquisition of BBVA USA in 2021. On the other side of the coin, some large banks hold the stance that they can eventually scoop up customers of fintechs looking for premium services once their usage has reached a scale where they feel comfortable serving them directly.

Pursuing a new business model may result in an identity crisis for certain financial institutions. However, in some ways, completely avoiding the trend is akin to avoiding the inevitable. Consider that nearly one in three consumers plan to address significantly (12%) or somewhat (18%) more of their financial needs through fintech providers over the next 12 months, rising to 48% of Gen Z and 43% of millennial respondents, according to 451 Research's Quantifying the Customer Experience 2022 survey.

Banking as a service

Banks generally participate in embedded finance by offering their bank charter "as a service." This allows the fintech provider to offer fundamental banking services, such as making nationwide loans and taking FDIC-insured deposits, with the underlying regulated financial institution supporting these use cases.

In some instances, banks will offer up their balance sheet to support lending use cases, and many choose to specialize in a certain area, for example, lending, cryptocurrency or cards. It is not uncommon for a fintech to work with multiple banks to address specific needs. Affirm Holdings Inc., for instance, partners with Evolve Bank & Trust for the Affirm Card while leveraging Cross River Bank and Celtic Bank Corp. for financing.

Several trends are emerging around banking-as-a-service collaboration, including:

Banking-as-a-service platform vendors. Small and midsize banks will often partner with a banking-as-a-service platform vendor — such as Synctera Inc., Treasury Prime Inc. or Unit — to support the various technology and infrastructure needs of fintech providers. This can be thought of as a middleware layer that abstracts some of the inherent complexity and operational overhead involved in bank and fintech integrations. It is common for banking-as-a-service platform providers to work with multiple banks, both for redundancy and to support specific use cases. For instance, Unit counts various bank partners, including Pacific West Bank, Piermont Bank and Thread Bank. Small fintechs tend to work with banks via banking-as-a-service platform vendors, while large, sophisticated fintechs often partner with operationally mature banks directly.

Banks creating banking-as-a-service divisions. Banks such as Westpac Banking Corp., Skandinaviska Enskilda Banken AB (publ), Standard Chartered PLC, Synovus Financial Corp. and Goldman Sachs Group Inc. have made recent moves in this direction by spinning up their own banking-as-a-service units underpinned by a custom-built technology platform that enables direct fintech collaboration. Several banks, including Green Dot Corp. and Cross River Bank, have long been operated as "full stack" banking-as-a-service providers. NatWest Group PLC has taken an interesting approach in that it entered into a strategic partnership with fintech startup Vodeno Group in 2022 to create a new UK banking-as-a-service entity, which is 82% majority-owned by NatWest Bank.

Banking-as-a-service platform vendors becoming (and buying) banks. A few banking-as-a-service platform vendors, such as Germany-based Solaris SE and UK-based Griffin Financial Technology Ltd., have secured their own banking licenses to operate as full-stack providers in Europe. However, we should point out that the vendors in these examples, especially Solaris, are not keen on building balance sheets. They leverage securitization to transfer lending assets/risks to investors, which could be banks themselves. There have also been select examples of banking-as-a-service platform vendors acquiring, or being formed through acquisitions of, banks. Column provides an intriguing example, in that the vendor launched after it acquired and modernized the tech stack of Northern California National Bank. BM Technologies Inc., on the other hand, recently called off its planned acquisition of First Sound Bank following a lengthy regulatory approval process.

It is important for both banking-as-a-service platform vendors and partner banks to build out technology, systems and processes to have oversight into their fintech partners' operations and the kinds of activities taking place. Because banks are regulated entities, they must ensure their fintech partners are operating in a compliant manner — providing customers with necessary disclosures, preventing fraud and abiding by necessary laws, for example, debt collection — or risk putting their bank charter in jeopardy. In the US, the Office of the Comptroller of the Currency (OCC) has been increasing its scrutiny of bank-fintech collaborations. In October 2022, it announced the establishment of the Office of Financial Technology to bolster its focus on the trend.

The OCC's growing involvement with financial institutions partnering with fintechs is perhaps best illustrated by its 2022 run-in with Blue Ridge Bank, where it uncovered "unsafe or unsound practice(s), including those relating to third-party risk management, Bank Secrecy Act/Anti Money Laundering risk management, suspicious activity reporting, and information technology control and risk governance" pertaining to its fintech partnerships. Blue Ridge Bank later entered into an agreement with the OCC requiring it to enhance its compliance and oversight processes pertaining to its fintech partners. Most notably, the agreement requires Blue Ridge Bank to secure approval from the OCC for future fintech partnerships.

In a more recent example, the FDIC in March entered into a consent order with Cross River Bank in regards to what it believes to be "unsafe or unsound banking practices" related to Cross River's compliance with "applicable fair lending laws." The FDIC has required a number of actions for Cross River, including obtaining third-party assessments for its fair lending compliance and information systems, in addition to seeking non-objection from the FDIC for any new credit products or new partnerships with third-parties.

Recent regulatory actions send a signal to the rest of the banking sector that there is a greater need to enhance due diligence and risk management on fintech partners and to ensure ongoing monitoring and oversight of their operations. This should not be an opportunity banks stumble into without a formal strategy and operational buildout.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

451 Research is part of S&P Global Market Intelligence. For more about 451 Research, please contact 451ClientServices@spglobal.com.