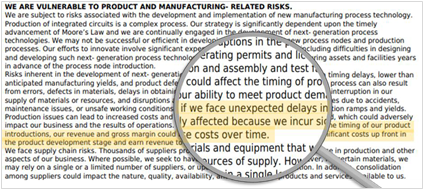

Company quarterly (10-Q) and annual (10-K) filings have traditionally been a vital source of information for investment decisions. However, the increasing length and complexity of these filings can result in investors overlooking new and important details in these reports. For example, Intel Corporation (“INTC”) updated the “Risk Factors” section of its 2017 10-K filing released on February 16, 2018 with the following: “if we face unexpected delays in the timing of our product introductions, our revenue and gross margin could be adversely affected” (Figure 1). Investors appeared not to have noticed this update as the stock climbed 5% in the week following the earnings release. INTC eventually disclosed a significant delay in the launch of its new 10-nanometer processor during its 2018 2Q earnings call held on July 26, 2018. The company’s stock dropped by 8% that day (despite earnings and revenue beats) and fell by another 6% over the next 3 months.

Figure 1: Intel Corporation 2017 10-K Risk Factors Section Excerpt

Source: Intel Corporation 10-K Filing. S&P Global Market Intelligence Quantamental Research. Data as of 02/28/2021.

This report uses three metrics (Minimum Edit Distance, Jaccard Similarity, and Cosine Similarity) to identify companies that made significant changes to the “Risk Factors” section of their filings. These metrics can serve as alpha signals or be used to quickly identify a pool of companies that require further investigation. Our findings include:

- Updates to risk disclosures may indicate a structural change in a company’s business or new threats to its existing businesses. A quintile portfolio strategy that buys (sells) companies with small (large) changes in the “Risk Factors” section of 10-K and 10- Q regulatory filings yields an annualized return of up to 5.36% (Table 1).

- Given that most companies make little or no changes to risk disclosures, a quintile approach may include companies with small changes in the short portfolio. A process that targets only companies with “significant” changes (outliers) in the short portfolio produces an annualized long-short return of 6.59% (Table 2).

- Information conveyed by changes to the risk disclosures by large cap companies are quickly incorporated into their stock prices, as large caps are more widely followed by analysts and receive more news coverage. Therefore, as shown in Table 3, the performance is stronger in the small cap space (6.42%) compared to the large cap segment (2.37%).

- Slow signal decay is consistent with the view that updates to risk disclosures act as a proxy for risks yet to be revealed, which will materialize over time. Annualized long-short return (3.32%) remains significant with a 12-month signal implementation lag (Table 4).