RatingsDirect® on S&P Capital IQ Pro

Reimagine your credit analysis workflow with the official source for S&P Global Ratings credit ratings and research

As the official source for S&P Global Ratings credit ratings and research, RatingsDirect combines this essential intelligence with comprehensive market data, credit risk indicators and dynamic visualization tools, all on a single platform.

Get the whole credit story, faster, from your desktop or on the go.

- Widest coverage with 1 million+ credit ratings outstanding

- Global, national and regional scale credit ratings on issuer and issue level

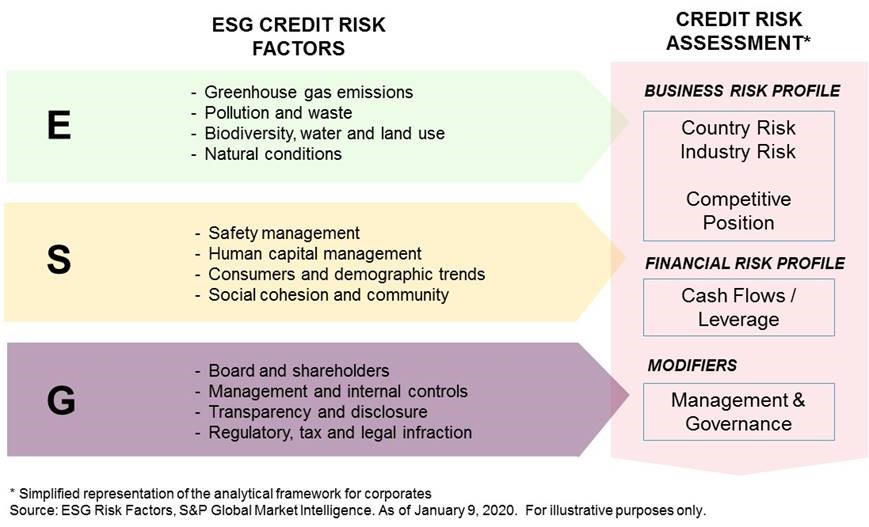

- Detailed research on issuer and issue level, economies, credit trends, hot topics (including Environmental, Social, and Governance [ESG]) and special reports

- Credit research in Chinese, Portuguese, Russian, and Spanish

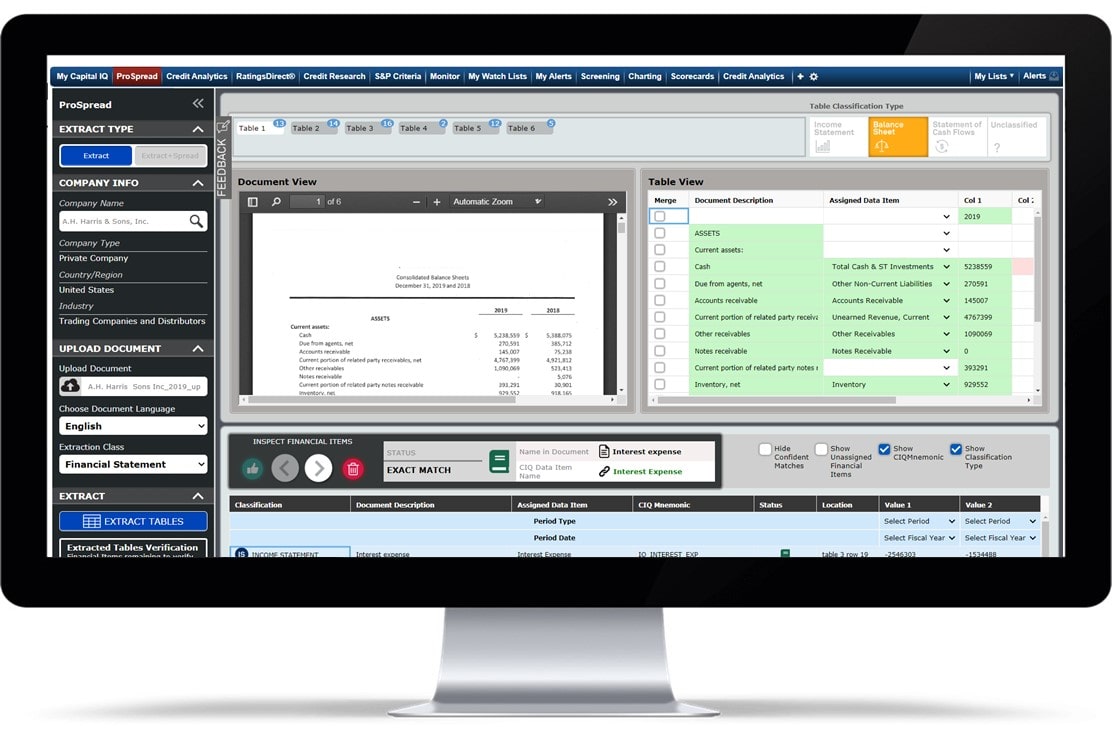

- Credit adjusted Income Statements, Balance Sheets and Cash Flow