Global inflation, increasing interest rates, continuing supply chain disruptions and the war between Russia and Ukraine are just a few of the issues challenging asset owners and risk managers around the world. Credit insurance and reinsurance firms are asked by senior management and regulators to conduct rigorous stress testing exercises to understand the shift in the risk profile of their portfolios under plausible yet volatile macro-economic scenarios. Having a robust scenario analysis framework in place for better risk management, risk pricing and capital planning purposes is more important than ever before.

This firm is a leading private markets reinsurance company, providing property, casualty, and specialty reinsurance coverage to insurers and reinsurers, globally. The firm manages a portfolio of credit risk for which they re-insure losses above a contractual excess threshold. The client uses several internal risk measurement and insurance premium pricing models. Inputs to these quantitative models include credit transition matrices, that are typically generated from historical information of rating agencies and from internal models’ credit score data.

![]()

Pain Points

The firm's current approach to risk management needed to be enhanced with forward looking analytical insights that would enable the risk management team to:

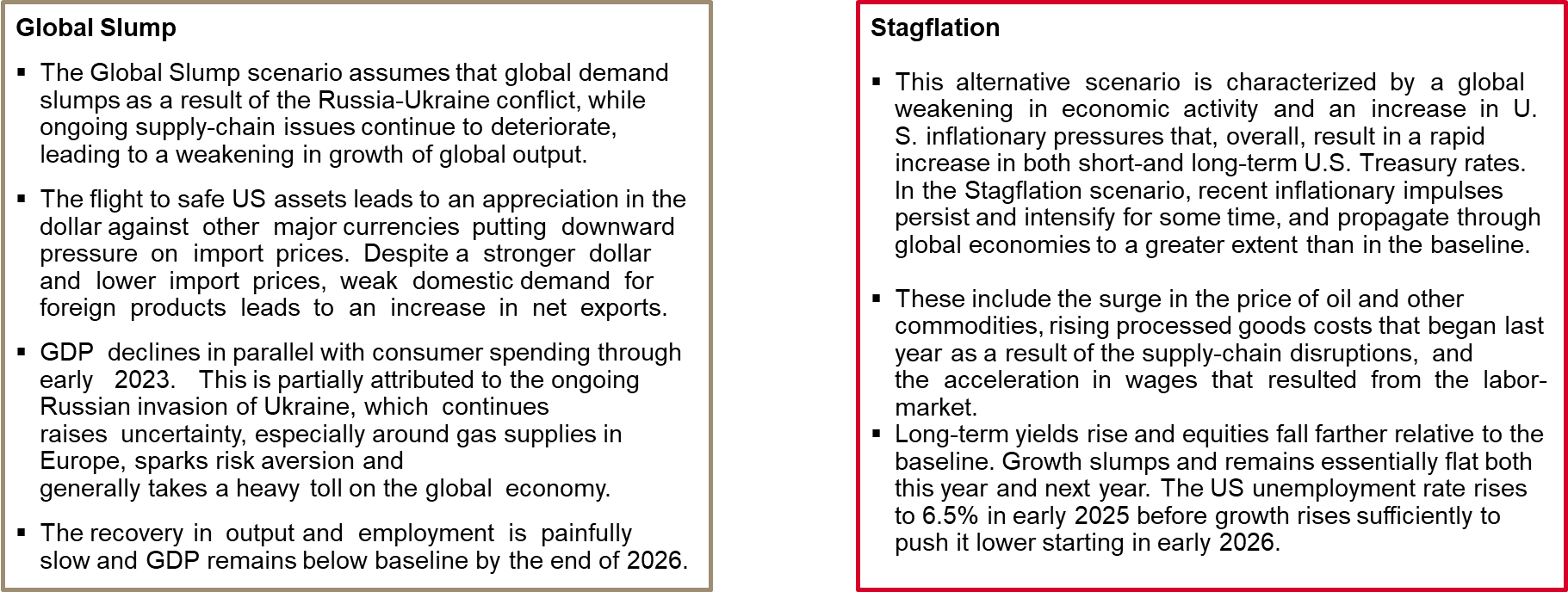

- Incorporate plausible, forward-looking, multi-year macro-economic scenarios to assess and manage downside risks in their credit reinsurance portfolio;

- Extend their analyses of historical credit migration and default rates to an objective view of future credit risk change based on actual behavior data from a reputable source;

- Apply a forward-looking, granular overlay to historical behavior to identify potential pockets of risk in different cross-sections of country and industry sectors.

![]()

The Solution

S&P Global Market Intelligence experts provided stressed credit transition matrices, which quantify the credit impact of economic downside scenarios using country and industry specific macro-scenario overlay models. Alternative economic scenarios are routinely generated by a team of economists using the Global Link Model (GLM). GLM also allows bespoke macro-economic scenarios, such as two described below to address portfolio specific vulnerabilities, as was the case with this client.

This approach allowed to complement more than 40 years of historical default rates and credit transition data from S&P Global Market Intelligence’s CreditPro®’s database of S&P Global Ratings’ issuer credit ratings changes for Corporates.

Country and industry specific credit transition matrices were then forecasted by running the Credit Analytics’ Macro-Scenario Model (MSM), which was trained on the historical statistical relationship observed between credit ratings’ changes and corresponding macro-economic conditions, to enable the credit risk management team to assess the impact of multiple downside scenarios on the default rates and credit transitions in the portfolio over the analysis horizon. Webservice is available for the model, allowing the results to be generated efficiently in batch.

This combined solution provided the credit risk team with insights needed to stress and model the credit reinsurance portfolio and quickly identify vulnerabilities within specific sectors relative to a baseline forecast. The project equipped the client credit risk team to:

|

Define and explore macro-economic implications of be-spoke events and shocks |

Model-based standard and bespoke scenarios assist financial institutions with all aspects of design, development, and quantification of macroeconomic and macro-financial variables necessary to measure risks, meet regulatory requirements, and comply with accounting standards such as CECL and IFRS 9. |

|

|

Understand the future evolution of default rates and credit transitions under each scenario |

Historical averages and scenario conditional values for default rates and credit migrations were used as inputs into portfolio and credit risk premium models. These credit default and migrations are based on 40+ years of S&P Global Ratings’ historical database and projections conditioned on user-selected macro-economic scenarios, over the chosen time-horizon. |

|

|

Identify industry-sectors most at risk and take relevant action |

Analysis is tailored and streamlined to assess the credit risk impact on country and industry specific exposures. |

![]()

Key Benefits

Client’s credit risk team leveraged Market Intelligence’s subject matter expertise in macro-economic scenario design, credit modeling, sector-specific data and technological innovation to improve the their credit risk assessment and pricing process. The solution set provided team members with an analytical solution that help them to review and price credit risk exposures in their portfolio based on plausible future macro-economic shocks on the downside. Furthermore, the client valued having access to:

- Clear documentation summarizing the narrative related to each macro-economic scenario, along with further analysis.

- Expected future default and credit migration rates at a granular, country and sector-specific level.

- A strong Product support team to discuss business needs, translate those to the scenario narratives and model methodology, and to interpret the results.

- Agile delivery supporting the quick integration of credit risk models into client’s risk management framework.