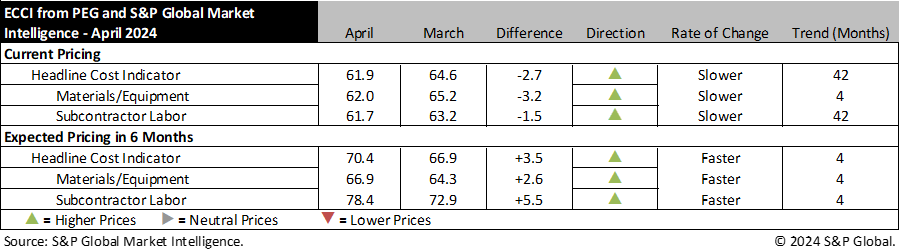

New York – April 24, 2024 – Engineering and construction costs increased again in April, according to the Engineering and Construction Cost Indicator from PEG and S&P Global Market Intelligence. The headline Engineering and Construction Cost Indicator, a leading indicator measuring wage and material inflation for the engineering, procurement and construction sector decreased 2.7 points to 61.9 this month; April’s reading is still well above the breakeven 50 mark, indicating prices continue to rise, though increases were slightly less widespread than last month. The sub-indicator for materials and equipment costs edged down 3.2 points to 62.0 while the sub-indicator for subcontractor labor costs fell to 61.7 in April from 63.2 in March.

The equipment and materials indicator continued to show rising prices in April. Only three of the 12 components increased compared to last month with an additional three remaining flat. Carbon steel pipe was unchanged and continues to remain in contractionary territory with a reading of 45.0, while pumps and compressors saw a minor decline to join shell and tube heat exchangers in neutral territory. Most of the other categories saw declines compared to last month. Transformers and electrical equipment each saw modest 6.8-point decreases, settling at 75.0, while both ocean freight categories saw double digit declines after two months of extremely high readings. The largest increase was seen for fabricated structural steel which saw an 18.6-point increase from contractionary territory up to a reading of 63.6.

“The outlook for construction steel has seen significant activity to start the year; prices rose in the first quarter given higher scrap costs but have remained stable ever since,” said Christos Rigoutsos, Senior Economist, S&P Global Market Intelligence. “Construction steel is currently overpriced, and we expect prices to slowly weaken. The construction outlook in the U.S. is buoyed by the Infrastructure Investment and Jobs Act projects that require the use of steel that has been melted, poured and rolled domestically. However, after 2024, demand is expected to wane, and prices will find a floor between $1,000 to $1,100/mt.”

The sub-indicator for current subcontractor labor costs saw a minor 1.5-point decrease compared to last month. The entirety of the decline was driven by the U.S. South region which saw significant decreases in all employment categories, bringing their readings in-line with all other regions. Offsetting some of the declines in the U.S. South, there were modest increases in some employment categories in each of the other U.S. geographic regions. There were no changes for any geography or employment category in Canada compared to last month.

The six-month headline expectations for future construction costs indicator increased modestly to 70.4 in April, the fourth straight increase. The six-month expectations indicator for materials and equipment came in at 66.9, 2.6 points higher than last month’s figure. Eight of 12 categories saw price expectations increase this month, while the other four saw declines. Fabricated structural steel, carbon steel pipe and alloy steel pipe each saw double digit increases to settle at readings between 63.6-68.2, a sizable shift from recent trends suggesting that the steel categories had near neutral expectations. The largest movements were in the ocean freight expectations which each saw declines of over 20-points. Routes from Asia to the U.S. settled at a neutral reading of 50.0 while Europe to the U.S. moved into contractionary territory at 45.0. This is a significant shift from recent expectations, illustrating that higher prices are no longer expected for six months from now.

The six-month expectations indicator for sub-contractor labor saw a 5.5-point increase to a reading of 78.4, continuing to show expectations for a tight labor market. Similar to the data for current pricing trends, the U.S. South region saw declines for each of the employment categories, moving them in line with the rest of the country. But the rest of the U.S. regions saw fairly large increases for almost all categories, resulting in higher total expectations. There were no changes for any geography or employment category in Canada compared to last month.

Respondents reported some shortages again this month for electrical equipment and labor, especially in the Gulf Coast area. Survey respondents also indicated that lead times for electrical equipment are driving schedules for major industrial projects.

To learn more about the Engineering and Construction Cost Indicator or to obtain the latest published insight, please click here.

# # #

About S&P Global Market Intelligence

At S&P Global Market Intelligence, we understand the importance of accurate, deep and insightful information. Our team of experts delivers unrivaled insights and leading data and technology solutions, partnering with customers to expand their perspective, operate with confidence, and make decisions with conviction.

S&P Global Market Intelligence is a division of S&P Global (NYSE: SPGI). S&P Global is the world’s foremost provider of credit ratings, benchmarks, analytics and workflow solutions in the global capital, commodity, and automotive markets. With every one of our offerings, we help many of the world’s leading organizations navigate the economic landscape so they can plan for tomorrow, today. For more information, visit www.spglobal.com/marketintelligence.

Media Contact :

Kate Smith, S&P Global Market Intelligence

P. +1 781 301 9311

E. katherine.smith@spglobal.com

Submitting your email above means you agree to the Terms and have read and understood the Privacy Policy