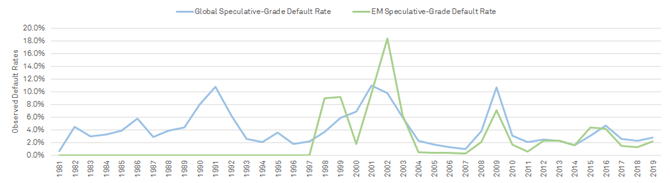

According to S&P Global Ratings research, extended coronavirus-containment measures are pushing the world into the deepest recession since the Great Depression, with a pace of deterioration this time that’s been a lot faster than in any previous crisis. The impact to emerging markets is severe with unprecedented capital outflows, tightening financing conditions, and pressured currencies.[1] A surge in defaults globally is already in motion and is expected to reach levels last seen in 2009 (following the Global Financial Crisis), in 2002 (Tech Bubble), and in 1990 (a US economic recession).

Figure 1: Global and Emerging Markets (EM) Trailing-12-Month Speculative-Grade Default Rate

Source: S&P Global Market Intelligence’s CreditPro®, data as of April 20, 2020

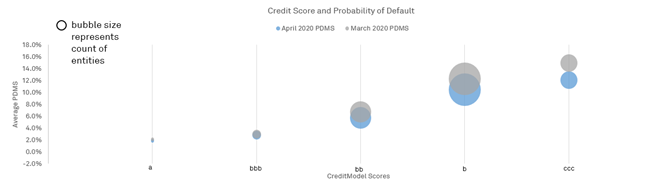

We used S&P Global Market Intelligence’s CreditModel™ (CM) and Probability of Default Market Signal (PDMS), from our suite of Credit Analytics statistical models, to assess the creditworthiness of 6,158 financial and non-financial corporates based in Central Asia, European Emerging Markets, Middle East and North Africa, Sub-Saharan Africa, and the Indian sub-continent (to better understand the models and the methodology employed in our study please refer to appendix 1 - models and methodology explained). [2] The credit landscape of our sample study is largely skewed towards the lower-end of the scoring spectrum (see figure 2 below). The bubble size in figure 2 represents number of entities, with those scored ‘b’ accounting for the largest share.[3] Such concentration indicates high credit risk of entities composing our sample study. Lower scores are more susceptible to negative credit pressure that the current environment is producing with higher vulnerability to adverse business, financial or economic conditions, and are the least likely entities to survive this crisis unscathed without any external support.

In the context of emerging markets, weaker credit scores takes an even more paramount importance as a result of unprecedented capital outflow, rollover risk and higher cost of funds. This view is validated by the market’s view, according to our PDMS model, with increasing probability of default (PD) as we go down that scoring spectrum (from ‘a’ to ‘ccc’). The emergence and spread of Covid-19 globally naturally triggered a negative pressure on asset values worldwide and on the markets sampled in this study, which however was further exacerbated by the drop in oil prices. A significant number of countries in our sample study rely heavily on revenues generated from oil exports to finance their budgets, especially infrastructure investments. Economic growth in such oil-exporting countries is therefore highly sensitive to the oil price landscape leading to capital outflow and hence stress on equity prices, and ultimately the market derived likelihood of default. We see a slight improvement in the overall default likelihood of the constituents of our sample study with PDs as of 29 March 2020 (the date of our last study, Developing Markets: Credit Memo, March 2020) higher than the PDs as of 20 April 2020. The moderate improvement of PD is further illustrated in figures 3 and 4.

Figure 2: Credit Risk Profile by Credit Score and Probability of Default

Source: S&P Global Market Intelligence; Credit Analytics CM and PDMS, blue bubble as of 20 April 2020, grey bubble as of 29 March 2020

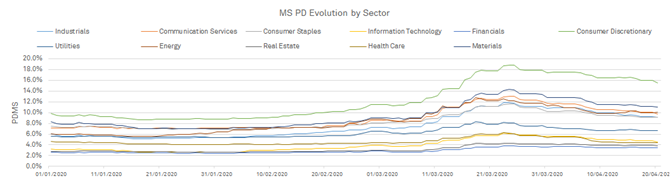

Figures 3 and 4 show a drop in PD around late March reflecting improved investor sentiment following what were acute capital outflows.[4] Improved sentiment is attributed to financial easing provided by the central banks in their respective markets, especially in dollar-currency liquidity on the back of swaps made available by the Fed to key emerging markets around late March.[5]

Looking at PDMS at the industry level (figure 3), most sectors continue to show high likelihood of default with the highest risk associated with Consumer Discretionary sector, a trend that is equally seen globally with investors fearing that non-essential spending will be severely hit. Materials and Energy, unsurprisingly, come second and third, respectively, in terms of PD and this is a result of weaker economic growth prospects, but also reflective of the nature of most economies in the sample study: (1) being highly dependent on import of raw materials from global markets and exposing them to supply chain risks; and (2) high dependence on export of commodities (oil, minerals, etc.) which exposes them to economic risks. The sector ‘Financials’ has the lowest PDMS, also unsurprisingly, with many academic and journalistic reports classifying this crisis as corporate credit risk, which banks are, to an extent, mitigated against thanks to capital having been built up following the global financial crisis. S&P Global Ratings continues to expect banks to show resilience during the Covid-19 breakout thanks to generally strong capital, substantial support from the public authorities, and the eventual rebound in the global economy, which itself is centered on the view that Covid-19 remains a temporary shock to the system rather than a long term structural issue. When assessing emerging market banks, S&P Global Ratings cites that while banks are “more exposed than developed market peers, [it] expect most will face an earnings rather than a capital shock, exacerbated by lower investor appetite and increasing funding cost for systems dependent on external financing”.[6]

Figure 3: PDMS Evolution by Sector

Source: S&P Global Market Intelligence, Credit Analytics PDMS as of April 2020, 2020

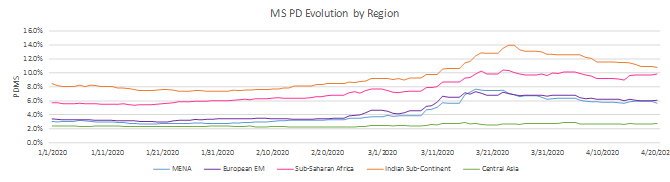

Looking at PDMS at the regional level (figure 4), we see the decreasing PDMS trend with Indian-based corporates showing less likelihood of default compared to levels seen in our March 2020 edition, but this is met with an increase in PDMS of Sub-Saharan based corporates. PD remains high for all regions (Central Asia shows a stable PD however this can be down to small size bias with only 10 entities forming the sample). The main attribution here is the systematic component denominating all emerging markets, mainly driven by severe capital outflows, lower oil prices, and higher cost of funds (see figure 6). According to Financial Times, the Institute of Internal Finance (IIF) estimates the cross-border outflows to be in region of USD95 billion in the first quarter of 2020, four times the amount that left in the same period after the start of the global financial crisis.3 Out of interest to confirm the systematic explanation of the PDMS curve of our sample universe, we undertook a statistical study to analyze the contribution of macro factors (GDP growth, Oil Prices) to the overall PD progression (summary graphs presented in Appendix 2 Panel Results of PDMS Macro-Variable Multi-Regression). The graphs clearly demonstrate, in line with the established expectations, high correlation of PD trends and the macroeconomic variables.

Figure 4: PDMS Evolution by Region

Source: S&P Global Market Intelligence, Credit Analytics PDMS as of April 20, 2020

Indian Sub-continent continue to have the highest overall PD. While the main attribution is the systematic risk, another attribution to this highlight is the construct of our sample study, not favoring Indian corporates who form circa 55% of our sample study with the majority of them engaging in high PD sectors, namely Consumer Discretionary, Materials, and Industrials. This compares unfavorably with, as a comparative example, our MENA sample having a concentration on low PD sectors, namely Financials. Nevertheless, even if we confine the analysis on an industry basis, we find Indian corporates with higher PD compared to other regional clusters in our sample (figure 5). For instance the average PDMS for Consumer Discretionary corporates in India is 17%, as of 20 April 2020 (19% as of 29 March 2020) compared to 12% in MENA (11% as of 29 March 2020). We have developed a heat map showing average PDs across sectors and regions (figure 6). The heat map confirms, to a large extent, a common sentiment that investors are sharing across sectors.

Figure 5 PDMS Heat Map Snapshot - Region and Sector

Source: S&P Global Market Intelligence, Credit Analytics CM and PDMS as of 20 April 2020

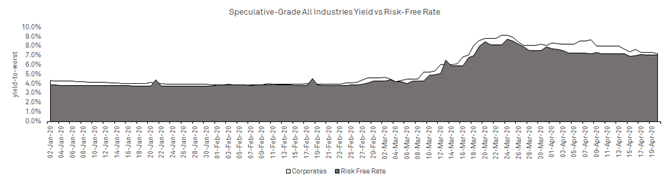

Beyond the PDMS curve, we take a look at the corporate yield curve of issuers from the sample study (figure 6), and confirm the same view of elevated risk that we start seeing escalating around late March, coinciding with the rise PDMS, unsurprisingly. The observed increase in yield is driven by the increase in the respective benchmark rates (sovereign USD issuance) and a widening of the spread. The rise in yield indicates higher risk of refinancing which can ultimately translate into delinquencies and ultimately defaults. We see a tightening of the spread around mid-April a few days after the Fed released its expanded liquidity into emerging markets.

Figure 6 Yield Curve

Source: S&P Global Market Intelligence, as of 20 April 2020

Click here for complimentary access to S&P Global Ratings research mentioned in our report.

Click here if you are interested in learning more about our Credit Analytics tools used in this analysis.

Appendix 1 – Models and Methodology Explained

Credit Analytics’ CM can generate credit scores for companies of all types including rated and unrated, public and private companies, globally. This becomes especially useful for our study that addresses a largely unrated market. We also use PDMS model, which uses stock price and asset volatility as inputs to calculate a one year PD. This helps us understand which corporates have experienced significant changes in default risk, based on market-derived signals. We conducted our analysis by generating medians from PDMS based on both sector and regional clustering. Combining CM and PDMS for our study helps in (1) ranking entities in absolute terms according to their long-term view of credit risk and (2) in mapping these scores to one year PD based on derived market signals.

Appendix 2 – Panel Results of PDMS Macro-Variable Multi-Regression

S&P Global Market Intelligence research

- “Industries Most and Least Impacted by COVID 19 from a Probability of Default Perspective March 2020 Update”, April 7, 2020

- “What’s the Market Sentiment Top Five Industries Impacted by COVID 19 from a Probability of Default Perspective”, March 16, 2020

S&P Global Ratings research

- “Credit Conditions Emerging Markets: Longer Lockouts, Heightened Risks”, S&P Global Ratings, April 23, 2020

- “Rising Credit Pressures Amid Deeper Recession, Uncertain Recovery Path”, S&P Global Ratings, April 22, 2020

- “How COVID-19 Is Affecting Bank Ratings”, S&P Global Ratings, April 22, 2020

- “Assessing The Coronavirus-Related Damage To The Global Economy And Credit Quality”, March 24, 2020

- “The Global Recession Is Likely To Push The U.S. Default Rate To 10%”, March 19, 2020

- “COVID-19 Credit Update: The Sudden Economic Stop Will Bring Intense Credit Pressure”, March 17, 2020

RatingsDirect® subscribers: Sign-in Here > to access the most up-to-date research from S&P Global Ratings.

External research

- “Bolsonaro, Brazil and the coronavirus crisis in emerging markets”, Financial Times, April 19, 2020

- “Fed sets up scheme to meet booming foreign demand for dollars”, Financial Times, March 31, 2020

- “How coronavirus became a corporate credit run”, Financial Times, March 2020

[1] “Rising Credit Pressures Amid Deeper Recession, Uncertain Recovery Path”, S&P Global Ratings, April 22, 2020

[2] We chose listed entities in select developing markets; we managed to generate CM scores for 5,674 entities while 484 remained unscored (“ns”) however they were associated with PDMS and hence we kept them in our study.

[3] Lowercase nomenclature is used to differentiate S&P Global Market Intelligence PD market signals [or credit model scores] from the credit ratings issued by S&P Global Ratings.

[4] “Bolsonaro, Brazil and the coronavirus crisis in emerging markets”, Financial Times, April 19, 2020

[5] “Fed sets up scheme to meet booming foreign demand for dollars”, Financial Times, March 31, 2020

[6] “How COVID-19 Is Affecting Bank Ratings”, S&P Global Ratings, April 22, 2020